Table of Contents >> Show >> Hide

- First, What Does “Cashing Out Home Equity” Even Mean?

- The 2025 Reality Check: Lots of Equity, Not-So-Cute Rates

- Option 1: HELOC (Flexible, Convenient… and Potentially Moody)

- Option 2: Home Equity Loan (Simple, Predictable, Less “Surprise!”)

- Option 3: Cash-Out Refinance (Big Move, Big Consequences)

- When Tapping Home Equity Can Be a Smart Move

- When Cashing Out Home Equity Is Usually a Bad Idea

- The Math That Matters: Don’t Compare Monthly Payments Only

- Tax Reality: Don’t Assume the Interest Is Deductible

- A Simple Decision Framework (No Financial Fortune-Telling Required)

- Alternatives to Cashing Out Equity (Sometimes Boring, Often Brilliant)

- Conclusion: Is Now the Time?

- Real-World Experiences: What Tapping Home Equity Looks Like in Practice (Composite Stories)

You know that smug feeling when your home value jumps and you suddenly feel like a real estate mogul?

Congratsyou’ve discovered home equity, the “wealth” you can’t actually use without paperwork, fees,

and a lender judging your credit score like it’s a reality show.

Still, the question is legit: Is now the time to cash out some home equity?

With homeowners sitting on a lot of equity, and borrowing costs no longer in the “basically free” era,

the right answer depends on what you’d do with the moneyand what it costs you to get it.

This is an in-depth, plain-English guide (with a little humor, because math is scary) to help you decide whether tapping

your equity makes sense, which option fits best, and how to avoid turning your house into a very expensive ATM.

First, What Does “Cashing Out Home Equity” Even Mean?

Home equity is the difference between what your home could sell for and what you still owe on your mortgage.

“Cashing out” means converting some of that equity into usable moneyusually by borrowing against your home.

There are three common ways to do it:

- HELOC (Home Equity Line of Credit): A revolving line you can draw from as neededoften with a variable rate.

- Home equity loan: A lump sum with a fixed payment scheduleoften a fixed rate.

- Cash-out refinance: You replace your existing mortgage with a larger one and take the difference in cash.

The key idea (and the part people forget at parties): you’re swapping “paper wealth” for real debt.

That debt has monthly payments, interest, and consequences if life gets messy.

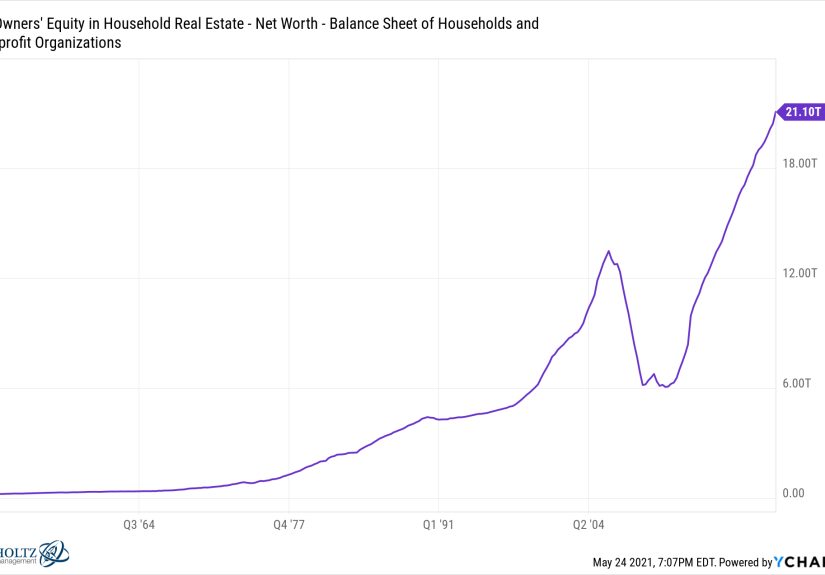

The 2025 Reality Check: Lots of Equity, Not-So-Cute Rates

Homeowners as a group still have substantial equity, even after the housing market cooled from its hottest moments.

Many borrowers have six figures of tappable equity sitting in their homes.

Meanwhile, mortgage rates have been hovering around the mid-6% range lately. That matters because the cost of accessing equity

is no longer “sure, why not?” money. It’s “let’s run the numbers twice, and then once more for emotional support.”

This creates a split reality:

-

If you have a low first-mortgage rate (think: locked in years ago), a cash-out refinance can be painful

because you’d refinance your entire balance into today’s higher rate. -

If you need a smaller amount, a HELOC or home equity loan can sometimes let you keep your original mortgage intact

while borrowing just what you need.

Option 1: HELOC (Flexible, Convenient… and Potentially Moody)

How it works

A HELOC works a bit like a credit card tied to your home: you’re approved for a limit, you borrow what you need,

and you pay interest on the amount you’ve drawn. Many HELOCs have a draw period (when you can borrow) and a repayment period

(when you pay it back).

Why people like it

- Flexibility for ongoing projects (renovations, tuition, phased expenses).

- Potentially lower upfront costs than a full refinance.

- You keep your original mortgage if you already have a great rate.

What to watch out for

- Variable interest rate risk: payments can rise if rates rise.

- “It’s there, so I’ll use it” temptation: flexible credit can become lifestyle creep in loan form.

- Payment shock when the repayment period starts (especially if you only paid interest early on).

Option 2: Home Equity Loan (Simple, Predictable, Less “Surprise!”)

How it works

A home equity loan gives you a lump sum upfront, usually with a fixed interest rate and fixed monthly payments

over a set term. You know exactly what you’re signing up for, which is refreshing in modern life.

Why people like it

- Fixed payments make budgeting easier.

- Good for one-time needs (debt payoff, a single renovation, a large planned expense).

What to watch out for

- Less flexibilityyou get the money once, not as-needed.

- Still secured by your home: miss payments long enough and it can become a serious problem.

Option 3: Cash-Out Refinance (Big Move, Big Consequences)

How it works

A cash-out refinance replaces your existing mortgage with a new, larger loan. You keep the house,

but you “reset” the mortgage balance and take cash for the difference (minus closing costs).

When it can make sense

- Your current mortgage rate is not dramatically lower than today’s rate, so refinancing the whole balance isn’t a huge penalty.

- You need a larger amount and want a single payment, fixed terms, and potentially a longer repayment window.

Why it can be a trap

- You pay today’s rate on your entire mortgage balance, not just the extra cash you want.

- Closing costs can reduce how much cash you actually receive.

- Turning other debt into mortgage debt can increase your foreclosure risk if your income gets disrupted.

Translation: this isn’t “free money.” It’s a strategic trade-off that needs a purpose and a plan.

When Tapping Home Equity Can Be a Smart Move

The best uses of home equity tend to have one thing in common: they improve your financial position or your life in a lasting way,

not just your weekend.

1) Home improvements that (actually) improve the home

Fixing a roof, replacing ancient HVAC, addressing foundation issues, or doing a thoughtful remodel can protect value

and make the home more functional. Bonus: using funds to substantially improve the home may matter for tax rules on interest.

2) High-interest debt consolidation (with guardrails)

If you’re carrying credit card debt at painful rates, a lower-rate equity loan can reduce interest costs.

But there’s a catch: you must stop the cycle. Consolidation only works if you don’t reload the cards.

3) Emergency liquidity (when you’re not already drowning)

A HELOC can function as a backup emergency lineespecially for homeowners with stable income and strong budgeting habits.

The goal isn’t to spend it; it’s to have access if something big breaks.

4) Life transitions with a clear payoff

Sometimes equity helps bridge a planned transitionlike covering costs during a job change, funding licensing for a higher-paying role,

or making a home accessible for aging relatives. The “smart” part is having a timeline and a repayment plan.

When Cashing Out Home Equity Is Usually a Bad Idea

Here’s the part that sounds boring but saves real money: don’t use your house to finance a vibe.

1) Lifestyle spending dressed up as “deserved”

Vacations, weddings you can’t afford, constant upgrades, a car that costs more than your futurethese can turn into years of payments.

Fun is great. Thirty-year fun financing is… less great.

2) Investing the proceeds because “markets always go up”

Borrowing against your home to invest can backfire if markets drop or stagnate for long stretches.

It’s one thing to invest with extra cash; it’s another to invest with money that puts your home on the line.

3) Income uncertainty or tight cash flow

Equity lending adds a monthly obligation. If your job is shaky or your budget is already stretched,

taking on more debt can create stress at the exact moment you need flexibility.

4) You’re near retirement and replacing “paid-off security” with debt

For many households, a paid-off (or nearly paid-off) home is a key retirement stabilizer.

Adding new payments late in the game can increase riskespecially with rising property taxes, maintenance,

or insurance in certain areas.

The Math That Matters: Don’t Compare Monthly Payments Only

A lender can make almost anything “affordable” by stretching the term. That doesn’t make it wise.

Focus on these decision points:

- Rate: fixed vs variable, and how it changes your risk.

- Total costs: interest + fees + closing costs.

- Term length: a lower payment can mean paying far more over time.

- What you’re refinancing: are you replacing a great mortgage rate with a worse one?

- Equity buffer: keeping meaningful equity reduces risk if prices soften.

A quick example (why cash-out refis can sting)

Let’s say you owe $300,000 on a mortgage at 3.0% and want $50,000 cash for a renovation.

If you do a cash-out refinance at ~6.2% on a new $350,000 loan, you’re not just borrowing $50,000 at the new rate

you’re borrowing the entire $350,000 at the new rate (plus closing costs).

If instead you keep your 3.0% mortgage and take a home equity loan for $50,000, you may pay a higher rate on that second loan,

but only on the $50,000not on your whole mortgage balance.

The “best” choice depends on rates available to you, your timeline, and whether you value payment simplicity over overall cost.

Tax Reality: Don’t Assume the Interest Is Deductible

A common myth: “Home equity interest is always deductible.” Not exactly.

In many cases, the deductibility of interest on home equity borrowing depends on how you use the funds.

If the money is used to buy, build, or substantially improve the home that secures the loan, interest may qualify

(subject to IRS rules and limits). If you’re using it for debt consolidation, tuition, or a business venture, the interest may not qualify.

Taxes shouldn’t be your only reason to borrow, but you should understand the rules so you’re not budgeting based on a deduction you can’t take.

A Simple Decision Framework (No Financial Fortune-Telling Required)

If you want a “wealth of common sense” approach, here’s a straightforward checklist:

Step 1: Name the purpose in one sentence

“I want to borrow $X to do Y by Z date.” If you can’t say it clearly, it’s probably not a disciplined plan.

Step 2: Choose the tool that matches the purpose

- Ongoing expenses (phased renovation) → HELOC might fit.

- One-time lump sum (single project, payoff) → home equity loan might fit.

- Large amount + need a single payment → cash-out refinance might fit (but compare carefully).

Step 3: Stress test your budget

Can you handle the payment if your income dips? If the HELOC rate rises? If your property taxes or insurance increase?

If you can’t survive a few “what ifs,” the loan is too big.

Step 4: Keep an equity cushion

Your home is not a day-trading account. Keeping meaningful equity reduces risk and preserves flexibility

if the housing market wobbles or life throws you a curveball.

Alternatives to Cashing Out Equity (Sometimes Boring, Often Brilliant)

- Reprice the project: do the renovation in phases instead of all at once.

- Build a cash buffer: a sinking fund can beat debt for planned expenses.

- Shop other credit wisely: a lower-cost personal loan can be safer than using your home as collateral.

- Negotiate and compare offers: rate shopping isn’t “extra,” it’s how you avoid overpaying.

Sometimes the best move is not borrowingit’s buying time, shrinking the goal, or finding a safer funding method.

Real-World Experiences: What Tapping Home Equity Looks Like in Practice (Composite Stories)

Below are composite “real-life” scenarioscommon patterns homeowners run into when deciding whether to cash out equity.

These aren’t individual stories; they’re blends of the kinds of decisions people make (and the lessons they learn).

1) The Renovation Relief (and the “scope creep” monster)

A couple plans a $40,000 kitchen refresh: cabinets, countertops, new lighting, done. They open a HELOC because it feels flexible

and it is. Then the contractor says, “If we’re opening that wall, you may as well upgrade the electrical.”

Then the appliances “need” to match. Then the floors look sad next to the new cabinets. Suddenly, the project is $70,000.

The upside: the house becomes more functional and enjoyable. The danger: a flexible credit line can quietly expand a budget.

The fix is simple (but not easy): a written cap, a strict “must-have vs nice-to-have” list, and the willingness to say,

“No, I will not finance a fancy faucet for the next decade.”

2) The Debt Domino (consolidation that worksonly if behavior changes)

A homeowner carries $25,000 in credit card debt after a medical bill + job disruption combo. A home equity loan offers a lower rate,

predictable payments, and an emotional win: “Finally, one payment instead of five.”

When this goes well, it’s because the homeowner closes the loop: they adjust spending, build a small emergency fund,

and stop relying on cards for surprise expenses. When it goes badly, the cards get paid off… then slowly refill.

That’s the domino effect: now you’ve got the equity loan payment and the rebuilt card balances.

The practical lesson: consolidation is a tool, not a cure. Pair it with a budget reset and automatic savings so the “why” doesn’t happen again.

3) The Low-Rate Lock-In (why some people avoid cash-out refis)

Another homeowner has a mortgage rate that looks like it came from a magical eralow enough to feel untouchable.

They want $50,000 for a renovation, but a cash-out refinance would reprice their entire mortgage at today’s higher rates.

They run the numbers and realize they’d pay far more interest over time than they expectedjust to get that $50,000.

So they take a smaller second loan instead, or they phase the remodel in stages. The experience here is about preserving a valuable asset:

a low-rate mortgage can be worth protecting, even if that means slower progress on the project.

4) The “Hidden Costs” Surprise (fees, insurance, and reality)

A homeowner expects to walk away from a cash-out refinance with a neat pile of cash. Then closing costs show up,

and the net proceeds are smaller than planned. Around the same time, their homeowners insurance renews at a higher premium.

The monthly budget gets squeezed from multiple directions, not just the loan payment.

The big takeaway: borrowing decisions should include the full housing-cost picturemortgage payments, taxes, insurance,

and maintenance. Equity can help you solve a problem, but it can also tighten your monthly cash flow if you don’t plan for the “extras.”

Bottom line from the trenches

The best “experiences” with home equity have three ingredients: a clear purpose, conservative borrowing (with an equity cushion),

and a repayment plan that still works if life gets a little bumpy. If you borrow like a grown-up, equity can be a tool.

If you borrow like your house is a scratch-off ticket, it can become a long, expensive lesson.