Table of Contents >> Show >> Hide

- What “Social Security Income Limits” Really Means

- The Limit Most People Mean: Working While Collecting Social Security

- The Good News Nobody Hears First: Withheld Benefits Are Not Lost Forever

- What Counts as Earnings and What Does Not

- The Special Monthly Rule in Your First Year of Retirement

- The Other “Income Limit”: Taxes on Social Security Benefits

- The Payroll Tax Limit Is a Different Animal

- Medicare Premiums Can Create Another Income Surprise

- Do Not Mix Up Retirement Benefits and SSI

- Smart Ways to Handle Social Security Income Limits

- What These Limits Feel Like in Real Life

- Final Takeaway

If you have ever tried to understand Social Security income limits and felt like the government handed you three different rulers, two calculators, and one very judgmental worksheet, you are not alone. The phrase Social Security income limits sounds simple, but it actually covers several different rules. One limit affects people who claim retirement benefits early and keep working. Another determines whether part of your benefits may be taxable. A third controls how much of your wages are subject to Social Security payroll tax. Then, just for extra seasoning, Medicare and SSI bring their own income rules to the party.

That is why so many people ask the same question in slightly different ways: How much can I earn while on Social Security? Will my benefits be reduced? Will my taxes go up? And why does every answer seem to start with, “Well, it depends”? The good news is that once you separate these rules, the picture gets much clearer. This guide breaks down the most important Social Security income limits in plain English, using real-world examples, practical planning tips, and enough nuance to be helpful without turning into a tax-law sleep aid.

What “Social Security Income Limits” Really Means

When people search for information about Social Security income limits, they are usually talking about one of four things:

| Rule | 2026 Amount | Why It Matters |

|---|---|---|

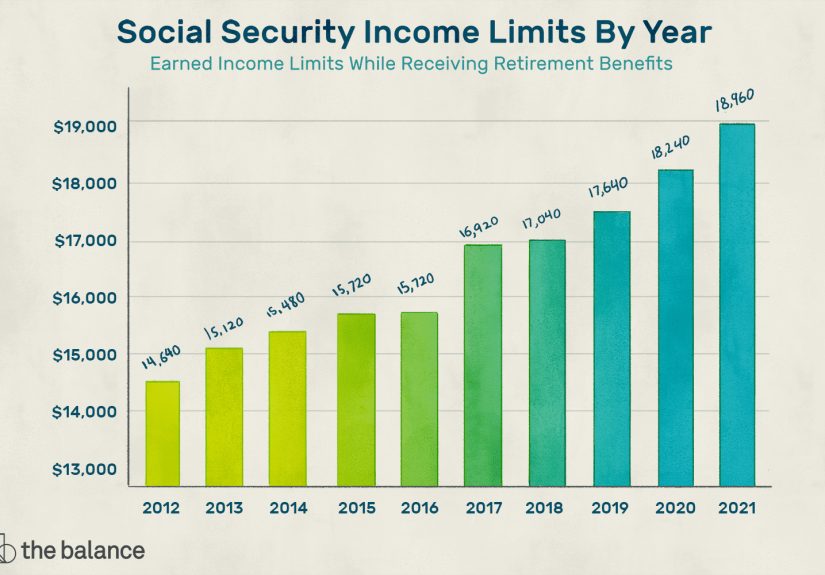

| Earnings limit if you are below full retirement age all year | $24,480 | Your benefits may be temporarily withheld if work earnings go above this amount. |

| Earnings limit in the year you reach full retirement age | $65,160 | A more generous limit applies, and only earnings before the month you reach full retirement age count. |

| Federal tax thresholds for Social Security benefits | $25,000 single / $32,000 joint | These thresholds determine whether part of your benefits may be subject to federal income tax. |

| Social Security payroll tax wage cap | $184,500 | This is the maximum amount of earnings subject to the Social Security payroll tax in 2026. |

| Medicare Part B IRMAA starting point | $109,000 single / $218,000 joint | Higher income can increase Medicare premiums, which many retirees confuse with a Social Security cut. |

Right away, here is the key point: these limits do not all do the same thing. One affects benefit withholding, one affects taxes, one affects payroll contributions while you are working, and one affects Medicare costs. If you mix them together, Social Security starts to look like a haunted spreadsheet. If you separate them, it starts to make sense.

The Limit Most People Mean: Working While Collecting Social Security

The most talked-about rule is the retirement earnings test. This rule applies if you start collecting Social Security retirement benefits before full retirement age and continue to work.

For 2026, the basic rules are straightforward:

If you are under full retirement age for the entire year

You can earn up to $24,480 in 2026 before Social Security starts withholding part of your benefits. If you earn more than that, the Social Security Administration withholds $1 in benefits for every $2 you earn above the limit.

Example: Say you are 63, you already claimed retirement benefits, and you earn $34,480 from a part-time job in 2026. That is $10,000 over the limit. Social Security would withhold $5,000 in benefits for the year. Annoying? Yes. Gone forever? No. More on that in a minute.

If you reach full retirement age during 2026

The rule gets much friendlier. In the months before you reach full retirement age, you can earn up to $65,160. If you go over that amount, Social Security withholds $1 in benefits for every $3 above the limit.

Example: Suppose you reach full retirement age in September 2026 and earn $71,160 before that month. You are $6,000 over the limit, so Social Security would withhold $2,000 in benefits. Once you hit full retirement age, the earnings test stops applying.

After full retirement age

Once you reach full retirement age, there is no earnings limit for Social Security retirement benefits. You can work full time, part time, seasonally, or obsessively, and your wages will not reduce your retirement checks under the earnings test.

For many current retirees, full retirement age is 67, especially for people born in 1960 or later. For others, it falls somewhere between 66 and 67 depending on birth year. That age matters because it changes the rules from “watch your earnings” to “carry on.”

The Good News Nobody Hears First: Withheld Benefits Are Not Lost Forever

One of the biggest myths around Social Security income limits is that if benefits are withheld because you worked too much, that money is simply gone. Not exactly.

Social Security says that when you reach full retirement age, your benefit is recalculated to give you credit for months in which benefits were withheld because of the earnings test. In plain English, that means the government is not tossing your money into a volcano. Your monthly benefit can be adjusted upward later to reflect the months you did not receive checks.

This is why many advisers describe the earnings test as a timing issue rather than a pure penalty. That does not make it fun in the year it happens, but it does make it less catastrophic than many retirees fear.

What Counts as Earnings and What Does Not

This is the part where many people get tripped up. For the retirement earnings test, Social Security does not count every dollar that flows through your life.

What usually counts:

- Wages from a job

- Net earnings from self-employment

- Bonuses

- Commissions

- Vacation pay

What usually does not count:

- Pensions

- Annuities

- Investment income

- Interest

- Dividends

- Veterans benefits

- Government or military retirement benefits

That distinction matters a lot. If you sell stock, collect rental income, take IRA withdrawals, or receive pension payments, those amounts generally do not count toward the retirement earnings test. They may matter for your taxes, and they may matter for Medicare premiums, but they do not usually trigger Social Security benefit withholding under the work rule.

In other words, Social Security is mostly focused on earned income from work, not the entire circus of your retirement cash flow.

The Special Monthly Rule in Your First Year of Retirement

There is another wrinkle that can actually help people: the special earnings limit rule, often called the first-year rule.

This rule exists because many people retire midyear. If Social Security only looked at total annual earnings, someone who worked a full-time job for part of the year and then retired could appear to have earned “too much,” even though they genuinely retired later in the year.

So Social Security also looks at certain monthly limits in the first year you retire:

- If you are under full retirement age all year in 2026, you may be considered retired in any month your earnings are $2,040 or less.

- If you reach full retirement age in 2026, you may be considered retired in any month your earnings are $5,430 or less before the month you reach full retirement age.

This rule can help someone who had high wages earlier in the year but then truly stepped away from work. It is one of those useful Social Security details that rarely makes it into casual conversation, which is a shame because it can save people real money.

The Other “Income Limit”: Taxes on Social Security Benefits

Now we move to a completely different question: When are Social Security benefits taxable? This is not the same as the earnings test. It is a federal income tax issue, not a benefit-withholding rule.

The IRS uses something called combined income. Generally, that is your adjusted gross income, plus any nontaxable interest, plus half of your Social Security benefits.

For federal taxes, these are the thresholds most people watch:

- Single, head of household, or qualifying widow(er): if combined income is more than $25,000, part of your benefits may be taxable.

- Married filing jointly: if combined income is more than $32,000, part of your benefits may be taxable.

Then the ranges climb from there:

- For many single filers, combined income from $25,000 to $34,000 can make up to 50% of benefits taxable.

- Above $34,000, up to 85% of benefits may be taxable.

- For joint filers, $32,000 to $44,000 can make up to 50% of benefits taxable.

- Above $44,000, up to 85% of benefits may be taxable.

That last part is commonly misunderstood. “Up to 85% taxable” does not mean an 85% tax rate. It means up to 85% of your benefit amount may be included in taxable income, and then your regular tax rate applies to that taxable amount. Big difference. Very big. Put down the panic calculator.

Another important detail: Supplemental Security Income (SSI) is not the same as Social Security retirement benefits, and SSI payments are not taxable like retirement benefits are. If someone says, “Social Security income limits,” you should always ask which program they actually mean.

The Payroll Tax Limit Is a Different Animal

There is also a Social Security limit that matters mostly while you are still working: the taxable wage base. In 2026, the maximum amount of earnings subject to the Social Security payroll tax is $184,500.

That means if you are an employee, you pay the 6.2% Social Security tax on wages up to $184,500. Your employer pays the matching 6.2%. If you are self-employed, you cover both halves through self-employment tax. Earnings above that ceiling are not subject to the Social Security portion of payroll tax.

But here is the important distinction: this is not the same thing as the retirement earnings test. It does not determine whether benefits are withheld because you claimed early. It simply determines how much of your wages are taxed for Social Security purposes and how much of your earnings can count toward future benefit calculations.

Also, Medicare does not use the same cap. Medicare tax continues on all earnings, which is why high earners sometimes assume Social Security has “no limit” when in reality they are thinking of Medicare.

Medicare Premiums Can Create Another Income Surprise

Retirees often notice a smaller Social Security net payment and assume the earnings test is to blame. Sometimes the real culprit is Medicare.

In 2026, the standard Medicare Part B premium is $202.90 per month. But higher-income beneficiaries can pay more through IRMAA, the Income-Related Monthly Adjustment Amount. For 2026, Medicare looks at your 2024 modified adjusted gross income. If that amount was above $109,000 for an individual or $218,000 for a married couple filing jointly, you may owe a higher Part B premium, and possibly a higher Part D premium as well.

This does not mean Social Security cut your benefit because you worked too much. It means your Medicare premiums rose because of prior-year income. Different rule, same headache, identical confusion.

Do Not Mix Up Retirement Benefits and SSI

Social Security retirement benefits and SSI are cousins, not twins. SSI is a needs-based program for people with limited income and resources, and its income rules are separate from retirement benefit rules.

For 2026, SSI rules are different enough that they deserve their own file folder. A person generally must have less than $1,014 a month in unearned income to receive SSI, while a couple may qualify with less than $1,511 a month in unearned income. Because not all earned income is counted, a person already receiving SSI may be able to earn up to $2,073 a month, or $3,067 for a couple, and still potentially receive SSI payments.

So if you are researching Social Security income limits, make sure you know whether your question is about retirement benefits, SSDI, or SSI. Same agency, very different math.

Smart Ways to Handle Social Security Income Limits

If you want to avoid nasty surprises, a little planning goes a long way.

- Know your full retirement age. That one date changes everything about the earnings test.

- Separate earned income from other income. Wages and self-employment earnings matter for the retirement earnings test; pensions and investments usually do not.

- Watch timing if you are retiring midyear. The special monthly rule can be valuable in the first year you retire.

- Remember that taxes are a different issue. You might avoid benefit withholding and still owe taxes on benefits if your combined income is high enough.

- Look two years back for Medicare IRMAA. A spike in prior income can come back later through higher premiums.

- Keep working strategically if your earnings history is uneven. Social Security checks your record annually, and additional work can replace low-earning years in your 35-year earnings history.

The broader lesson is simple: do not plan retirement around a single headline number. Social Security has multiple income-related rules, and each one answers a different question. The people who do best usually are not the ones who know every regulation by heart. They are the ones who know which rule applies to their situation.

What These Limits Feel Like in Real Life

On paper, Social Security income limits look neat and tidy. In real life, they tend to show up in much messier ways. Take the experience of someone like Linda, who claimed benefits at 62 because she was burned out, only to discover three months later that she still liked having money more than she disliked meetings. She picked up part-time consulting work, assumed her Social Security would stay the same, and then got a notice that some benefits would be withheld because her work income pushed her over the annual earnings limit. Her first reaction was classic: “Wait, nobody said there would be math.” What helped was learning that the withheld amount was not necessarily gone forever and that her benefit would later be recalculated.

Then there is someone like Marco, who retired in July after a long career in sales. For the first half of the year, he made a full salary. For the second half, he barely worked at all. He panicked because his annual income looked way too high for someone collecting Social Security. But the special monthly rule changed the story. Because he was truly retired later in the year and had low earnings in those months, he was not hit as hard as he feared. His experience is a good reminder that annual numbers do not always tell the full story.

Another common experience belongs to couples who are surprised by taxes rather than withholding. Denise and Howard, for example, may think their Social Security is “safe” because one spouse no longer works. But then IRA withdrawals, interest income, and half of their Social Security benefits combine in a way that pushes them into the range where part of their benefits becomes taxable. Nothing was wrong. Nothing was miscalculated. They simply ran into a different income rule than the one they had been watching.

High earners often run into a different kind of confusion. Someone still earning a strong salary may notice that Social Security tax stops being withheld after a certain point in the year and assume that means all payroll-related limits have vanished. Not so. That is the wage cap at work, not a signal that every government rule has gone on vacation. Medicare tax keeps going, and if that same person later claims Social Security early, the retirement earnings test is a separate issue altogether.

And then there are retirees who see a smaller net Social Security deposit and immediately blame work income, when the real issue is Medicare premiums. A one-time capital gain, Roth conversion, property sale, or unusually large withdrawal from retirement accounts can echo into the future through IRMAA. The benefit itself did not shrink; the deductions coming out of it got larger.

The lived experience of Social Security income limits is this: most problems do not come from the rules being impossible. They come from the rules being easy to confuse. Once people understand whether they are dealing with earned income limits, tax thresholds, payroll caps, SSI rules, or Medicare premium adjustments, the fog usually clears. Retirement still has enough moving parts to keep your calendar busy, but at least your Social Security questions stop feeling like a pop quiz written by accountants with a mischievous streak.

Final Takeaway

If you remember only one thing, make it this: there is no single master rule called “the Social Security income limit.” There are several separate limits, and each one affects your money differently. The 2026 earnings test limits decide whether benefits may be temporarily withheld if you claim early and keep working. Federal tax thresholds determine whether part of your benefits may be taxable. The wage cap decides how much of your work income is subject to Social Security payroll tax. Medicare and SSI add their own income rules on top.

Once you know which limit applies to you, planning gets much easier. And that is the real win here. Social Security may never be glamorous, but it does become a lot less mysterious when you stop treating every income rule like it came from the same spreadsheet tab.