Table of Contents >> Show >> Hide

- Why return expectations matter (more than your “hot take”)

- The three big building blocks of future returns

- “Lower your expectations” doesn’t mean “give up”

- Stocks: a simple way to think about the next decade

- Bonds: brush up on the math (because bonds actually obey it)

- Putting stocks + bonds together: what a “balanced” forecast looks like

- U.S. vs. international: diversification is still not canceled

- How to use return expectations without turning them into fan fiction

- Conclusion: common sense beats clairvoyance

- Experience Notes: What This Looks Like in Real Life (About )

If investing had a customer service desk, the #1 complaint would be: “Excuse me, I was promised 10% a year and a

lifetime supply of calm.” Unfortunately, markets don’t do promises. They do probabilities, mood swings, and the

occasional plot twist that makes you question every life choice you’ve ever madelike buying a “can’t miss” stock

because your cousin’s barber saw it on TikTok.

The good news: you can still build a smart plan. The better news: it doesn’t require predicting next quarter,

next year, or next Tuesday. It requires something rarer than a perfect market forecastreasonable return

expectations going forward, based on what we can observe today: yields, valuations, inflation, and how human

behavior tends to faceplant at the worst possible moment.

Why return expectations matter (more than your “hot take”)

Return expectations aren’t about winning an argument online. They’re about planning reality:

how much you need to save, how much risk you’re taking, and how likely you are to stay invested when the market

inevitably tries to shake you loose.

When expectations are too high, people under-save, over-risk, and panic-sell when the market stops cooperating.

When expectations are too low, people hoard cash, miss compounding, and later wonder why retirement feels like a

group project they didn’t study for.

The three big building blocks of future returns

Most long-term return forecastswhether they come from big asset managers, finance academics, or the “my gut says”

crowdend up circling the same core ingredients:

1) Starting yield (income) is the “boring engine”

For bonds, starting yield is a huge deal. Over long horizons, bond returns tend to resemble what you’re earning

in yield today (plus/minus price changes along the way). For stocks, the dividend yield is smaller than it used

to be, but it still matters. A low starting yield doesn’t doom returnsit just means more of your future result

has to come from earnings growth or valuation staying elevated.

2) Earnings growth (and economic growth) is the “muscle”

Over time, companies can return cash to shareholders (dividends/buybacks) and grow profits. That growth is tied

to productivity, innovation, competition, labor costs, and the economic environment. It’s real. It’s also

lumpybecause recessions exist, and businesses occasionally discover that “growth at any price” contains the word

“price” for a reason.

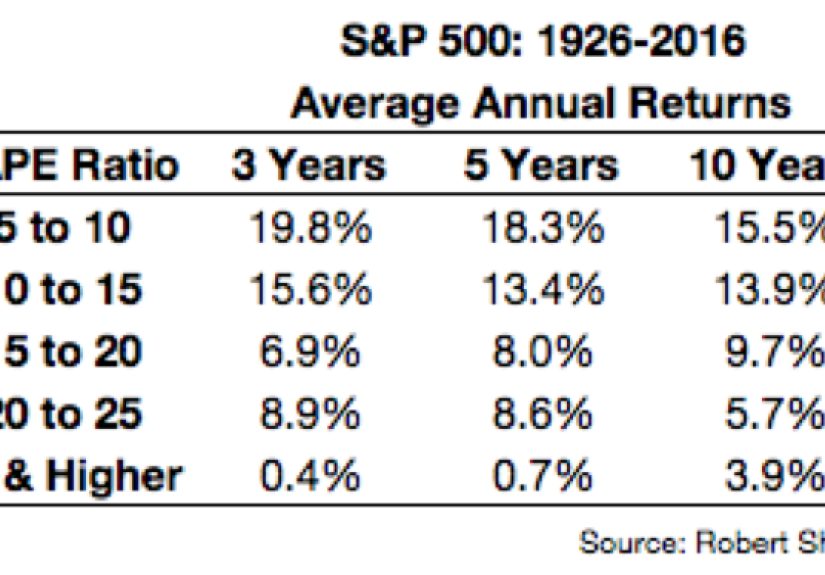

3) Valuation change is the “wild card”

Valuationhow expensive stocks are relative to earnings, cash flows, or dividendsdoesn’t predict next month. But

over longer horizons, it can heavily influence outcomes. When valuations start high, expected returns tend to be

lower; when valuations start low, expected returns tend to be higher. That’s not pessimism. It’s math wearing a

sensible sweater.

“Lower your expectations” doesn’t mean “give up”

One of the most useful messages in Ben Carlson’s “wealth of common sense” style is that long-term investors

should focus on reasonable expectations, not short-term predictions. A practical takeaway that shows up in many

institutional outlooks is this: U.S. stocks can still do fine, but starting valuations and low yields may imply

more muted forward returns than the blockbuster years investors have enjoyed in strong bull markets.

Vanguard, for example, has highlighted a muted U.S. stock return outlook over a 5–10 year horizon, with an

important nuance: the forecast is heavily influenced by the risk/return profile of large-cap tech and the

expectations embedded in current prices. In plain English: you can be bullish on innovation and still cautious

about what you pay for it.

Stocks: a simple way to think about the next decade

A classic “common sense” framework popularized by long-term, fundamentals-based investors breaks stock returns

into:

- Dividend yield (what you collect)

- Earnings growth (what the business becomes)

- Valuation change (what the market decides it’s worth)

Here’s how you might apply it without pretending you’re a fortune teller:

Example: a “reasonable” stock return range (not a guarantee)

Suppose the market’s dividend yield is roughly in the 1%–2% neighborhood and earnings grow at, say, 4%–6%

nominal over time. That gets you into a mid-single-digit ballpark before any valuation changes. If valuations

fall (multiple contraction), returns could be lower. If valuations rise further, returns could be higherbut

relying on that repeatedly is like building a retirement plan around finding a parking spot right in front of the

venue every single time.

The point is not to “call” the market. The point is to stop assuming that a recent streak of great returns is a

permanent feature of reality.

Bonds: brush up on the math (because bonds actually obey it)

Bonds are often misunderstood because people focus on what happened last year instead of what happens over the

next several years. Bond prices can swing when yields change, but the long-term expected return of a high-quality

bond portfolio is closely tied to its starting yield and the path of rates.

Why higher yields can be “good news” (eventually)

When yields are higher, new money gets invested at better rates, and the portfolio’s income improves. That’s one

reason many firms have argued that “bonds are back” in a world of higher starting yieldsespecially for investors

who want income and diversification benefits.

Term, credit, and the “paid to wait” question

Not all bonds have the same expected return. Duration (term) and credit risk matter. In systematic fixed income

research, the expected return of a bond can be viewed as its yield plus expected price change, and historically

wider term spreads and credit spreads have been associated with higher subsequent premia (though nothing is

guaranteed and spreads can widen for unpleasant reasons).

Putting stocks + bonds together: what a “balanced” forecast looks like

A balanced portfolio isn’t a personality trait. It’s a strategy for surviving the future without needing to be

right all the time.

One reason return expectations going forward have become more interesting (and more complicated) is that we’re

not in the same regime as the 2010s. Inflation shocks, rate shocks, and fiscal concerns can change how stocks and

bonds behave together. Yet major allocators still publish long-horizon assumptions for planningbecause having a

baseline is better than winging it.

A real-world planning anchor: long-term capital market assumptions

Large institutions publish “capital market assumptions” (CMAs) for a reason: pensions, endowments, and long-term

investors need return/risk estimates to set policy portfolios. These CMAs often imply:

- U.S. equity returns below long-term historical averages when valuations are elevated

- Fixed income returns closer to long-term norms when yields are more normal

- More relative attractiveness in non-U.S. markets when the U.S. is priced richly

For example, long-horizon assumptions from major firms have discussed how profits can offset valuations for

equities while higher yields and higher term premia can lift bond return forecastsleading to balanced portfolio

return expectations that remain positive even after strong equity years.

U.S. vs. international: diversification is still not canceled

If you’ve lived through a decade where U.S. stocks led the parade, international investing can feel like showing

up to a party where nobody knows your name. But valuation differences matter. When U.S. markets trade at a

premium and other regions trade at discounts, forward-looking expected returns can be higher abroadespecially

over long horizons.

This is one of those ideas that sounds obvious in theory and emotionally difficult in practice. Diversification

often feels “wrong” right before it looks smart.

How to use return expectations without turning them into fan fiction

Forward-looking returns are not a prophecy. They’re a planning tool. Here’s how to use them like an adult:

1) Plan with ranges, not point estimates

If your plan only works when stocks return exactly 10% every year, your plan is essentially a motivational

poster. Use conservative-to-base-to-optimistic ranges and stress-test outcomes.

2) Separate “need” from “want”

If you need a high return to meet goals, that’s a signal to adjust savings rate, timeline, or spending,

not to crank risk to 11 and hope the market cooperates.

3) Keep fees and taxes in the conversation

Net returns are what fund your life. A forecast of “6%” before fees and taxes can become “4%” faster than you can

say “expense ratio.” Don’t let a shiny expected return number distract you from controllable costs.

4) Rebalance like you mean it

After big moves, your portfolio can quietly become a different portfolio than the one you intended. Some

strategists have suggested rebalancing approaches that respond to volatility rather than just the calendarbecause

markets rarely send RSVP cards before they get dramatic.

5) Remember behavior is the hidden asset class

A “reasonable” return expectation that you can stick with beats an “aggressive” expectation you abandon at the

bottom. Many investors over-extrapolate recent performance: they feel optimistic after strong markets and

pessimistic after bad onesexactly backward from what long-term math suggests.

Conclusion: common sense beats clairvoyance

Return expectations going forward don’t require you to guess the next headline. They require you to respect the

starting point: yields, valuations, inflation, and the reality that markets don’t repeat on command.

The practical playbook is simple (not easy): diversify globally, keep costs low, use realistic ranges, and

rebalance with discipline. If you do that, you don’t need perfect forecastsyou need consistency. And consistency,

unlike predictions, actually compounds.

Experience Notes: What This Looks Like in Real Life (About )

Let’s translate all of this into the messy, human version of investingthe part where spreadsheets collide with

emotions and everyone suddenly becomes a macro strategist because they saw a scary chart.

The “I’m used to 20%” hangover

A very common experience after a strong multi-year run is return anchoring. Investors subconsciously treat the

recent past as a baseline: “Stocks return 15%–25% a year… right?” Then markets cool off, and the disappointment

feels personal. The better framing is: strong returns often pull future returns forward. When valuations rise and

yields fall, the market has already “spent” some of the easy gains. That doesn’t mean a crash is required. It

means the bar for future surprises gets higher.

The bond whiplash story

Another classic: someone buys bonds for stability, then rates rise and bond prices fall, and bonds get fired from

the portfolio like they committed a crime. Later, yields are higher, income is better, and the same person says,

“Wait… bonds are paying how much now?” This is the bond math lesson in the wild: price volatility can hurt in the

short run, but higher starting yields can improve the long-run return outlook. Many investors learn this only

after they’ve sold at the worst possible timeright before the “boring engine” starts working again.

The AI optimism trap

People can be both correct and early and still have a bad outcome. Investors often confuse “great technology” with

“great investment at any price.” AI may boost productivity and profits over time, but if the market already priced

in perfection, returns can be muted even while the technology succeeds. A common experience is holding a

high-flying theme, watching it stall, and deciding the theme was fakewhen the real issue was the purchase price

and expectations.

The awkward phase of diversification

Global diversification is emotionally difficult because it rarely pays off in a straight line. Investors will

hold international stocks through years of lagging performance, then quit right before the cycle turns. The “real

life” lesson: diversification often looks like regret before it looks like wisdom. When U.S. valuations are rich

and other markets are cheaper, expected returns abroad can be higherbut the payoff can arrive on a schedule that

is deeply inconvenient for impatient humans.

The quiet win: a plan that doesn’t break

The best experience investors report (usually after they’ve made every mistake once) is not “I predicted the

market.” It’s “I didn’t do anything stupid when things got weird.” They used reasonable return assumptions,

saved consistently, rebalanced, and let compounding do the heavy lifting. That’s the wealth of common sense in one

sentence: you don’t need to be a herojust don’t be your own portfolio’s villain.