Table of Contents >> Show >> Hide

- SPX vs. SPY: The Fast Answer

- What SPX Really Is

- What SPY Really Is

- The Biggest Differences That Actually Change Your Trading

- Which Traders Usually Prefer SPX?

- Which Traders Usually Prefer SPY?

- A Practical Example: Same Market View, Different Experience

- Common Mistakes Traders Make When Comparing SPX and SPY

- Final Verdict: SPX vs. SPY

- Trader Experience: What SPX and SPY Feel Like in the Real World

If you have ever stared at an options chain and wondered why some traders swear by SPX while others refuse to leave SPY, welcome to one of the most practical debates in options trading. On the surface, both products track the same neighborhood: large-cap U.S. stocks and the broad market mood swings that come with them. But under the hood, SPX and SPY are not twins. They are more like cousins who dress alike, borrow each other’s jokes, and then send you very different tax paperwork.

That difference matters. A lot. It affects contract size, assignment risk, how you hedge, how you manage expiration, and how much chaos can land in your account when a trade goes sideways at 3:58 p.m. In other words, choosing between SPX options and SPY options is not just about ticker preference. It is about choosing the tool that fits your account size, strategy, and tolerance for operational drama.

In this guide, we will break down the real-world differences between trading index options on SPX and trading ETF options on SPY. We will cover settlement style, exercise rules, tax treatment, position sizing, and trader use cases, with simple examples along the way. By the end, you should know which product makes more sense for hedging, premium selling, directional trades, and those inevitable moments when the market decides to test your emotional support levels.

SPX vs. SPY: The Fast Answer

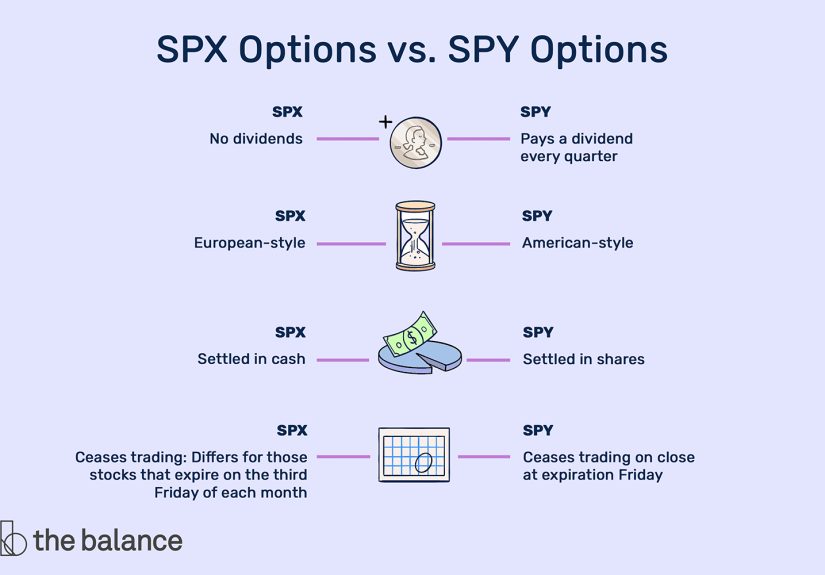

If you want the short version, here it is: SPX options are index options based on the S&P 500 Index itself, while SPY options are ETF options based on shares of the SPDR S&P 500 ETF Trust. That one structural distinction creates a chain reaction of differences.

- SPX options are usually larger, cash-settled, and European-style.

- SPY options are smaller, physically settled into ETF shares, and generally American-style.

- SPX is often favored by traders who want cleaner cash settlement, no early assignment, and potential tax advantages.

- SPY is often preferred by traders who want smaller sizing, flexible scaling, and an options market tied to a tradable ETF.

So if your priority is clean mechanics and institutional-style exposure, SPX often wins. If your priority is accessibility, granularity, and smaller account flexibility, SPY usually gets the nod.

What SPX Really Is

SPX options are tied to the S&P 500 Index, not to a fund you can buy and hold. That means you are trading options on an index value, not on shares of an ETF. There is no basket of stock shares delivered at expiration. There is no fund wrapper. There is just the index level, the contract multiplier, and the cash value created by the difference between strike and settlement.

This is why many experienced traders like SPX for hedging or premium strategies. It is broad-market exposure without the share-delivery headache. If a cash-settled SPX position finishes in the money at expiration, the account is credited or debited in cash. That can be much cleaner than waking up and discovering you now own or owe a pile of ETF shares because expiration played out a little too dramatically.

SPX is also big. One contract uses a $100 multiplier on the index level. So if the S&P 500 Index is at 5,800, one SPX contract represents about $580,000 of notional exposure. That is efficient, yes. Also humbling, yes.

What SPY Really Is

SPY, by contrast, is an ETF. It is the SPDR S&P 500 ETF Trust, a fund designed to track the price and yield performance of the S&P 500 Index before expenses. Because it is an ETF, its options behave like equity options. Standard contracts generally represent 100 shares of SPY.

That makes SPY much easier for smaller accounts to use. If SPY is trading at 580, one contract controls about $58,000 of notional value. That is still meaningful exposure, but it is far easier to size around than the much larger SPX contract.

The ETF wrapper brings a few extra quirks. SPY has distributions, it has an expense ratio, and because the options are tied to an actual tradable fund, contracts can be exercised into shares. That means traders in SPY options need to respect dividend timing, potential early assignment, and the possibility of ending up long or short shares after expiration or exercise.

The Biggest Differences That Actually Change Your Trading

1. Contract Size and Position Sizing

This is the first thing most traders notice. SPX is roughly ten times the notional size of SPY. That means one SPX contract can do the work of about ten SPY contracts when both are centered around the same market level.

For larger accounts, that is efficient. A portfolio manager hedging a sizable equity book may prefer one or two SPX contracts over juggling a cluster of SPY contracts. Fewer line items, broader exposure, simpler management.

But for smaller accounts, that same efficiency can feel like trying to park a cargo ship in a bike lane. SPY gives traders more precise scaling. Want to trim risk one notch at a time? SPY is usually better. Want to leg into spreads more gradually? SPY often makes life easier.

Hypothetically, if you wanted exposure close to $116,000 of the S&P 500, you could trade about two SPY contracts at a 580 price level. With SPX, one contract would overshoot that target by a mile. That sizing mismatch alone can decide the product choice.

2. Cash Settlement vs. Physical Settlement

SPX options are cash-settled. If they expire in the money, the result is a cash credit or debit based on the intrinsic value of the contract. No shares change hands. No surprise inventory shows up in your account.

SPY options are physically settled. If a call is exercised, shares are bought or delivered. If a put is exercised, shares are sold or delivered. This is normal for ETF options, but it changes the operational risk dramatically.

Imagine a trader who sells an SPY put spread and lets it sit too long into expiration week. If one side is assigned and the other expires differently than expected, the trader can end up with unwanted long or short ETF shares. That kind of surprise can turn a sleepy Friday into a very educational Monday.

For traders who value clean exits, SPX often feels more straightforward. For traders who are comfortable handling share exposure or who already trade the ETF itself, SPY can still work perfectly well.

3. European Style vs. American Style

This is another major fork in the road. SPX options are commonly European-style, which means they are exercised at expiration, not early. SPY options, as ETF options, are generally American-style, which means they can be exercised before expiration.

Why does that matter? Because early exercise means early assignment risk for short option sellers. And when dividends enter the chat, that risk gets louder.

With SPY, an in-the-money short call can be assigned before expiration, especially around the ex-dividend date. Traders who sell covered calls or call spreads on SPY need to watch that calendar. A short option that looks harmless on Thursday afternoon can become an assignment issue before you finish congratulating yourself for collecting premium.

With SPX, early exercise risk is removed from the equation. That does not make the trade risk-free, of course. Price risk is still very real. But at least the contract is not hiding a surprise share-delivery plot twist.

4. Tax Treatment

This is one of the most discussed reasons traders choose SPX. Broad-based index options such as SPX can fall under Section 1256 treatment, which is often summarized as the 60/40 rule: 60% long-term capital gains treatment and 40% short-term treatment, regardless of holding period, assuming the trader and strategy qualify.

SPY options are ETF options, so traders generally think about them under the framework used for equity and ETF options rather than broad-based index options. In practical terms, many active traders view SPX as potentially more tax-efficient than SPY. That said, this is where every smart article says the same sentence, and for once the article is right: tax details depend on your circumstances, so confirm the rules with a qualified tax advisor.

Still, the tax difference is not a small footnote. For high-frequency options traders or larger accounts, it can materially affect after-tax returns. A trade that looks equal on the screen may not be equal on the tax form.

5. Expiration and Settlement Nuances

Traders often lump “expiration” into one neat mental folder, but SPX and SPY can behave differently around settlement timing. Standard SPX contracts have long been associated with special settlement procedures, while weekly index variants and ETF options often line up differently. The key lesson is simple: never assume all expirations work the same way just because the chart looks familiar.

This matters most when you hold positions into the final trading window. SPX traders need to know exactly how the contract settles. SPY traders need to know exactly what happens if the option is automatically exercised into shares. In both products, the final hour rewards precision and punishes casual optimism.

Which Traders Usually Prefer SPX?

SPX tends to appeal to traders who want broad S&P 500 exposure in a more professional-grade package. That includes:

- Portfolio hedgers who want index protection without disturbing the stock positions they already hold.

- Premium sellers who dislike early-assignment risk.

- Active traders who care about potential Section 1256 treatment.

- Larger accounts that can handle the bigger notional size efficiently.

SPX can be especially attractive for traders who think in portfolio terms instead of single-position terms. It behaves more like a pure market overlay than a tradable equity substitute.

Which Traders Usually Prefer SPY?

SPY often makes more sense for traders who want flexibility and smaller increments. Common examples include:

- Smaller accounts that need finer control over size.

- Directional traders who want to build into positions gradually.

- ETF traders who already use SPY shares and want options on the same instrument.

- Spread traders who prefer the familiarity of standard equity-option mechanics.

SPY is often the more approachable gateway for traders moving from stock options into index-linked products. It is familiar, liquid, and easier to scale. That matters. The “best” product is not the fanciest one. It is the one that fits the trader using it.

A Practical Example: Same Market View, Different Experience

Let’s say a trader is moderately bullish on the S&P 500 and wants to sell a put spread. The market view is identical whether the trade is placed in SPX or SPY. But the experience can be very different.

In SPX, the trader may use one larger spread, benefit from cash settlement, and avoid early assignment risk. At expiration, the result is a cash outcome. Clean and direct.

In SPY, the trader may use several smaller spreads to fine-tune exposure. That offers flexibility. But if the trader mishandles expiration or ignores assignment risk, the position can morph into ETF share exposure. Same view, same strategy family, different mechanics, different operational stress.

This is why experienced traders do not just ask, “What do I think the market will do?” They also ask, “How do I want this trade to behave if I am right, wrong, or late?”

Common Mistakes Traders Make When Comparing SPX and SPY

Assuming They Are Interchangeable

They are related, but they are not interchangeable. Similar market exposure does not mean identical contract behavior.

Ignoring Position Size

Traders sometimes choose SPX because it sounds more sophisticated, then realize the notional exposure is larger than their risk plan can comfortably support.

Forgetting Dividend Risk in SPY

Short SPY calls near ex-dividend dates deserve respect. Many assignment surprises are less “black swan” and more “calendar negligence.”

Holding Too Casually Into Expiration

Expiration is not a suggestion. It is a process with rules, and those rules differ by product. Learn them before the position learns them for you.

Focusing Only on Pre-Tax Returns

A trade that looks identical on a gross basis can feel different after taxes. Serious traders compare after-tax outcomes, not just premium collected.

Final Verdict: SPX vs. SPY

If you want larger notional exposure, cash settlement, no early assignment, and potential tax advantages, SPX options are often the stronger choice. If you want smaller size, easier scaling, and the familiarity of ETF options, SPY options may be the better fit.

There is no universal winner in the SPX vs. SPY debate. There is only the better tool for the job in front of you. Professional traders often prefer SPX because the mechanics are elegant and efficient. Many retail traders prefer SPY because the sizing is practical and the learning curve is friendlier. Both choices are rational.

The smartest move is not picking the “cooler” ticker. It is choosing the contract that matches your capital, your strategy, and your ability to manage what happens at expiration. In options trading, elegance is nice. Compatibility is better.

Trader Experience: What SPX and SPY Feel Like in the Real World

After enough time around index options, most traders stop thinking about SPX and SPY as abstract products and start thinking about them as different personalities. SPX feels like the clean, efficient professional in a tailored suit. SPY feels like the flexible, practical workhorse that always shows up. Both can do the job. They just make you work differently.

Traders who start with SPY usually appreciate how manageable it feels. The size is easier to digest, especially when you are still learning how spreads move, how implied volatility changes pricing, and how quickly delta can stop being your friend. SPY lets you make mistakes in smaller pieces. That is not glamorous, but it is incredibly valuable. A lot of traders build real skill in SPY because the product allows repetition without forcing oversized exposure.

Then many of those same traders eventually look at SPX and realize why experienced options sellers keep talking about it. The first time you avoid share-delivery weirdness at expiration, the appeal becomes obvious. The first time you do not have to babysit early-assignment risk on a short call around a dividend date, it becomes even more obvious. SPX feels less cluttered. You are trading the market view, not the ETF plumbing.

That said, SPX can also punish sloppiness faster because the contract is bigger. Traders often discover that a strategy they “understand” in SPY suddenly feels very different when the notional size is multiplied. A spread that seemed comfortably small in SPY can become emotionally loud in SPX. The chart did not change. The trader’s heartbeat did.

Another common experience is that SPY tends to teach operational discipline, while SPX tends to reward structural discipline. SPY makes you respect dividends, exercise mechanics, and share settlement. SPX makes you respect size, settlement timing, and index-specific expiration details. If you trade both long enough, you begin to understand that product selection is part of risk management, not just a routing decision.

Many traders eventually settle into a simple pattern: SPY for smaller trades, scaling, and tactical experimentation; SPX for larger hedges, cleaner premium structures, and broad market exposure without the share-delivery mess. That is often the most mature conclusion. Not “Which one is best forever?” but “Which one is best for this exact job?”

In real trading life, that question is the one that matters. The market does not hand out bonus points for using a more sophisticated ticker. It rewards traders who understand their tools. And that is the real lesson from SPX vs. SPY. The better you understand the mechanics, the less likely you are to confuse a good market idea with a bad product choice.