Table of Contents >> Show >> Hide

- Financial Custodian, Explained Like You’re Busy

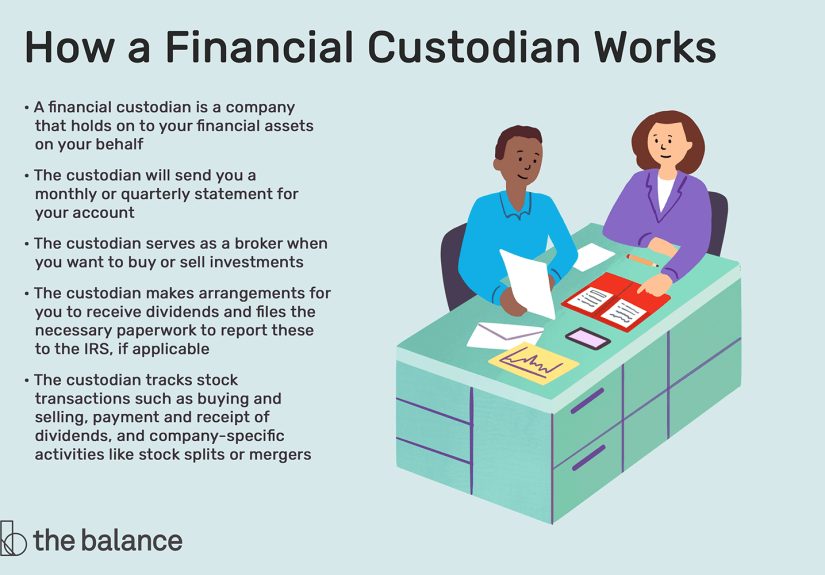

- What a Financial Custodian Actually Does

- Common Types of Financial Custodians (And Where You’ll Run Into Them)

- Custodian vs. Adviser vs. Trustee vs. Clearing Firm: Don’t Mix These Up

- How Financial Custodians Are Regulated (The Big U.S. Guardrails)

- Why You Should Care: Real Risks Custodians Help Reduce

- How to Choose a Financial Custodian (Checklist You Can Actually Use)

- Red Flags: When “Custody” Gets Sketchy

- FAQ: Quick Answers About Financial Custodians

- Real-World Experiences With Financial Custodians (About )

- Conclusion

If you’ve ever opened a brokerage account and wondered, “So… where is my money actually sitting?”congrats, you’ve stumbled into the world of

financial custodians. A financial custodian is the grown-up in the room who’s responsible for holding, safeguarding, and accounting for

financial assets like stocks, bonds, mutual funds, cash, and sometimes alternative investments.

Think of a custodian like the backstage crew at a concert. You’re watching the show (your portfolio), but they’re the ones making sure the lights turn on,

the doors stay locked, and nobody walks off with the instruments. The best part? When custodians do their job right, you barely notice they existwhich is

exactly what you want from someone guarding your financial stuff.

Financial Custodian, Explained Like You’re Busy

A financial custodian is a firmusually a bank, broker-dealer, or specialized custodian bankthat holds

assets on behalf of a client. “Client” can mean an individual investor, a retirement plan, a trust, an investment adviser’s customers, or even an institution

like a pension fund.

Custody matters because it creates separation: the person making investment decisions isn’t necessarily the same entity physically (or electronically) holding

the assets. That separation can reduce fraud risk, improve recordkeeping, and help regulators verify that assets exist where they’re supposed to exist.

What a Financial Custodian Actually Does

Custody sounds like “they hold my stocks,” but the real job is a whole bundle of unglamorous tasks that keep the financial plumbing from exploding:

Safekeeping and Asset Segregation

Custodians maintain accounts that identify who owns what, track positions, and (in regulated contexts) help keep customer assets separate from the firm’s own

operating money. This separation is a big deal when firms failbecause “that’s mine” is much easier to prove when the records are clear.

Trade Settlement and Cash Movement

When you buy a stock, it doesn’t teleport into your account instantly. Custodians (often working with clearing systems and counterparties) help ensure the

trade settles properlymeaning cash goes out, securities come in, and the transaction is recorded correctly.

Statements, Confirmations, and Tax Forms

Custodians generate account statements and transaction confirmations, and many issue tax documents such as 1099 forms for taxable brokerage accounts. In other

words: they’re the reason you can’t pretend you “forgot” about that one trade you made at 2 a.m.

Corporate Actions and Income Collection

Dividends, bond interest, stock splits, tender offers, proxy votingcustodians coordinate a lot of this behind the scenes. If a company pays a dividend, the

custodian helps credit it to the right accounts.

Retirement Account Administration (Sometimes)

In IRAs and certain retirement arrangements, custodians may also handle contribution tracking, required minimum distribution reporting, beneficiary

administration, and paperwork that helps the account stay compliant with rules.

Common Types of Financial Custodians (And Where You’ll Run Into Them)

1) Brokerage Custodians

This is what most people picture: the brokerage where you invest (or the firm behind your investing app) acts as the custodian of your securities and cash.

Sometimes there’s an introducing broker (the “front end”) and a clearing/carrying broker (the “back office”) that actually holds custody and handles

settlement.

2) Custodian Banks

Large banks provide custody services for institutions and high-net-worth clients, including “global custody” where a firm coordinates custody across multiple

countries through sub-custodians. This can include portfolio reporting, foreign exchange services, and specialized safekeeping.

3) Retirement Account Custodians

An IRA custodian is a financial institution that holds IRA assets and administers the account. Many mainstream brokerages and banks serve this

role. If you’ve opened a Traditional IRA or Roth IRA at a major brokerage, you’ve already chosen a custodian (even if you never interviewed them like a

reality TV contestant).

4) Custodial Accounts for Minors

“Custodial account” can also mean a legal arrangement (often under UGMA/UTMA rules) where an adult manages assets for a child until the child reaches

the age of majority. In this setup, the adult is the “custodian” (the responsible person), while the financial firm still serves as the institution holding

the assets.

5) Custody in the Investment Adviser World (RIAs)

Registered Investment Advisers (RIAs) may manage your investments, but many do not physically hold your assets. Instead, client assets are kept at a separate

firm that serves as a qualified custodian, and the adviser trades or manages the account through granted authorization.

Custodian vs. Adviser vs. Trustee vs. Clearing Firm: Don’t Mix These Up

Financial terms love to sound identical while meaning totally different things. Here’s the quick “who does what” map:

Financial Custodian

Holds and safeguards assets, maintains records, and supports settlement/reporting.

Investment Adviser (RIA or similar)

Provides advice or discretionary management. Often does not hold your assets directly; instead, the assets sit with a custodian.

Trustee

A trustee has fiduciary responsibility to manage assets for beneficiaries according to a trust document. A trustee may use a financial custodian to hold and

administer assets.

Clearing / Carrying Firm

A clearing firm processes trades, handles settlement, and often provides custody and back-office services for introducing brokers. If your investing app feels

“too small to be holding billions,” that’s because it may be using a larger clearing/custody partner behind the curtain.

How Financial Custodians Are Regulated (The Big U.S. Guardrails)

In the U.S., custody is closely tied to investor protection rules. The exact rulebook depends on the type of firm and account, but these are the themes you’ll

see again and again: segregation, recordkeeping, verifiability, and account statements.

“Qualified Custodian” Requirements for Investment Advisers

In the investment-adviser context, the SEC’s custody framework requires advisers with custody of client funds or securities to maintain them with a

qualified custodian, typically a bank or registered broker-dealer, among other categories. The goal is simple: client assets should be held at

a legitimate, regulated institution in properly identified accounts.

You may also hear about proposals to expand or modernize custody requirements. Regulatory ideas evolve, and not every proposal becomes a final rule. The

practical takeaway for everyday investors: when you work with an adviser, ask where your assets are custodied and whether you receive statements

directly from that custodian.

Broker-Dealer Customer Protection Expectations

Broker-dealers that hold customer funds or securities operate under customer protection requirements designed to safeguard those assets and reduce the risk of

misusing customer property. While the details can get technical fast, the investor-friendly concept is: your brokerage isn’t supposed to treat your

securities like its personal piggy bank.

SIPC vs. FDIC: The Insurance Alphabet Soup

Custody is also where people get tripped up on protections:

-

SIPC (Securities Investor Protection Corporation) generally applies to securities and cash held at a SIPC-member brokerage if the firm fails

and customer assets are missing. It’s about the custody function, not market performance. -

FDIC insurance applies to bank deposits (like checking/savings), subject to rules and limits. FDIC does not insure stock market losses, and

it doesn’t insure your brokerage portfolio just because your brokerage has the word “bank” somewhere in its corporate family tree.

Many brokerages also use “cash sweep” programs that move idle cash into bank deposit accounts or money market funds. The protection (FDIC vs. SIPC vs. neither)

depends on where the cash is actually held and the product typeso the disclosures matter.

Why You Should Care: Real Risks Custodians Help Reduce

1) Fraud and “Where Did the Money Go?” Risk

Separating advice/management from custody makes it harder (not impossible, but harder) for a bad actor to fabricate statements or quietly move assets. If you

get statements from an independent custodian, you’re less reliant on “trust me, bro” accounting.

2) Operational Errors

Most financial disasters aren’t movie-villain heists; they’re messy operational mistakes. Custodians provide standardized systems for settlement, recordkeeping,

and reporting that reduce the odds of chaos when markets move fast.

3) Firm Failure

If a brokerage firm becomes insolvent, custody safeguards and protections like SIPC are designed to help customers recover their property (within limits and

eligibility rules). That doesn’t mean you’re immune to hassle, but it’s better than “good luck, hope you kept screenshots.”

How to Choose a Financial Custodian (Checklist You Can Actually Use)

Whether you’re picking a brokerage, evaluating where your adviser custodies assets, or selecting a custodian for a retirement or custodial account, use this

short list:

Confirm the Custody Arrangement

- Who is the custodian (name the specific firm)?

- Are assets held in your name, or in an appropriately titled account for your benefit?

- Do you receive statements directly from the custodian (not only from an adviser)?

Understand Protection and Coverage

- Is the brokerage a SIPC member (and what does SIPC coverand not cover)?

- If cash is swept to banks, which banks, and how does FDIC coverage apply?

- Do they provide any additional private “excess” insurance, and what are the exclusions?

Evaluate Costs the Honest Way

- Custody may be “free,” but check for trading fees, account fees, wire fees, margin rates, and cash management spreads.

- If you use an adviser, understand advisory fees separately from custodian costs.

Service and Practical Features

- How easy is it to transfer assets in or out?

- Do they support the investments you want (ETFs, mutual funds, bonds, options, alternatives)?

- Do they offer beneficiary tools and decent customer support for life events (death, divorce, name changes)?

Red Flags: When “Custody” Gets Sketchy

- You can’t clearly identify which regulated firm holds your assets.

- You only receive statements created by the adviser, not by the custodian.

- Withdrawals or transfers are oddly difficult, slow, or “need special approval.”

- Promises of guaranteed returns or “risk-free” performance (markets do not sign those contracts).

- For digital assets: vague custody terms, unclear segregation, or missing disclosures about protections.

FAQ: Quick Answers About Financial Custodians

Is a financial custodian the same as a bank?

Not always. Banks can be custodians, but broker-dealers and specialized custodians can also hold assets. The “right” custodian depends on the account type and

regulatory context.

Can an investment adviser be my custodian?

Some advisers have custody in certain situations, but many advisers intentionally use an independent qualified custodian to hold client assets. The key is

transparency: you should know where the assets are held and receive custodian statements.

Does SIPC protect me if my investments drop in value?

No. SIPC isn’t a “bad market” warranty. It’s primarily designed to help return missing securities and cash in a brokerage failure, subject to rules and limits.

What about a custodial account for my child?

In a custodial account (often under UGMA/UTMA rules), the money generally belongs to the child, but an adult custodian manages it until the child reaches the

legal age in your state. The brokerage firm still serves as the financial custodian holding the actual assets.

Real-World Experiences With Financial Custodians (About )

Most people don’t “experience” a custodian the way they experience a restaurant or a video gamecustody is more like plumbing. You only think about it when

something leaks, clogs, or needs an upgrade. Still, investors tend to share a few common custody-related moments that make the concept feel very real, very

quickly.

One of the biggest wake-up calls happens during an account transfer. An investor switches brokerages (maybe for lower fees, better tools, or a

less annoying app interface), and suddenly they learn that transfers are a choreography between custodians. The smooth version looks like: submit a transfer

request, wait a few days, watch assets move over, done. The not-so-smooth version looks like: a missing cost basis, a mutual fund that can’t transfer “in kind,”

or a fraction of a share that gets liquidated and shows up as cash later. People often come away thinking, “Ohthis is a real system with real rails, not magic.”

Another common experience shows up when someone starts working with a financial adviser. A good adviser will explain, “Your assets stay at

this custodian. You’ll get statements from them. I manage the portfolio, but I don’t ‘hold’ the money in my desk drawer.” That sentence can be oddly

comforting. Clients like seeing that the adviser’s role (decision-making) and the custodian’s role (holding/reporting) are separate. It feels like the financial

version of having both a lock and a security cameradifferent tools, same goal: fewer unpleasant surprises.

Parents opening a custodial account for a minor often describe a “wait, it’s really theirs?” moment. They may deposit birthday money or invest

for college, then learn that the assets legally belong to the child and must be used for the child’s benefit. Some parents love the structure and simplicity.

Others realize they need to think ahead: when the child reaches the age of majority, the account becomes theirs to control, which can be either empowering or…

creatively terrifying, depending on the teenager.

Retirement savers run into custodian reality during beneficiary changes or after a family death. The custodian’s paperwork, verification steps,

and beneficiary tools can make an emotionally hard time either slightly easieror significantly more frustrating. People remember whether the custodian had

clear checklists, responsive support, and clean online processes. They also remember delays, repeated document requests, and “We can’t accept that form unless it’s

signed in blue ink under a full moon.” (Okay, maybe not the moon part, but you get the vibe.)

Finally, many investors have a learning moment around cash protection. They assume cash in a brokerage is “bank insured,” then discover that

protection depends on whether cash sits as a bank deposit via a sweep program or as cash in the brokerage account. That experience usually leads to better

habits: reading the cash management disclosures, understanding SIPC vs. FDIC, and keeping large balances intentional rather than accidental.

The pattern across these experiences is simple: a custodian is most valuable when life gets complicated. Transfers, big life events, and high-stress markets are

exactly when strong custody systemsgood records, clear ownership, and reliable processingstop being boring and start being essential.

Conclusion

A financial custodian is the institution that holds and safeguards your financial assets, tracks ownership, supports settlement, and provides

the reporting that makes investing function like a system instead of a rumor. Whether you’re investing through a brokerage, working with an adviser using a

qualified custodian, or managing a custodial account for a child, custody is the behind-the-scenes structure that helps protect your assets and prove they’re

yours. Pick custodians the way you pick locks: not because you expect disaster every day, but because you want the boring stuff to stay boring.