Table of Contents >> Show >> Hide

- What Episode 59 Is Really About

- Why Every Market Correction Feels Different

- Why a Shallow Recession and a Plain-Vanilla Bear Market Can Be Healthy

- The Economy Is Hard to Read Because It Sends Mixed Signals

- The Alpha Fantasy: Why Smart Institutions Still Think They’re Special

- Money, Happiness, and the Lottery Problem

- The Practical Lessons From Animal Spirits Episode 59

- Experiences From Living Through a Late-Cycle Market

- Conclusion

Some podcast episodes age like milk. Others age like a sturdy pair of boots: maybe a little scuffed, but still useful when the road gets messy. Animal Spirits Episode 59: Late Cycle belongs in the second category. Released at a moment when investors were nervously refreshing brokerage accounts and trying to decide whether “late cycle” meant “be careful” or “run for the hills,” the episode captured a mood that shows up in markets again and again.

That is why this episode still works. Ben Carlson and Michael Batnick were not just talking about one ugly stretch in stocks. They were talking about the timeless investor habit of mistaking turbulence for the end of civilization. Markets wobble, headlines panic, experts suddenly sound like doom poets, and the phrase of the week becomes a full-blown personality trait. In late 2018, that phrase was late cycle.

This episode lands because it mixes macroeconomics, market history, behavioral finance, and just enough everyday absurdity to keep the conversation human. One minute the discussion is about whether the economy is nearing a slowdown. The next minute it drifts into happiness, lottery fantasies, alpha-chasing institutions, and the weird ways people anchor their decisions. That blend is exactly what makes Animal Spirits work: it treats investing not as a spreadsheet contest, but as a real-life sport played by emotional, overconfident, habit-driven humans.

What Episode 59 Is Really About

At first glance, Late Cycle sounds like a classic market-timing episode. The title practically begs for ominous background music. But the deeper point is not “sell everything and hide in canned beans.” It is that investors love labels because labels make uncertainty feel tidy. Early cycle, mid-cycle, late cycle, recession, recovery. Those words are useful, but they are also dangerous when people start treating them like prophecy instead of framework.

The late-cycle phase usually describes an expansion that is still alive but clearly not sprinting anymore. Growth is still there, yet it tends to moderate. Labor markets often look tight. Inflation pressure can rise. Interest rates may be higher than they were earlier in the cycle. Earnings growth can cool off. Credit conditions may start to matter more. None of that automatically means disaster. It simply means the easy part of the expansion is usually behind you.

That distinction matters. Investors often hear “late cycle” and translate it into “game over.” But late cycle is not the same thing as recession. It is more like the last hour of a long road trip. You are still moving, the destination has not arrived, and everyone is a little more irritable than they were three states ago.

Why the Phrase “Late Cycle” Gets So Much Attention

Because it sounds smart, slightly ominous, and wonderfully flexible. If the market keeps rising, late cycle can mean “still room to run, but watch your footing.” If the market falls, late cycle suddenly becomes “see, I told you.” It is the Swiss Army knife of market commentary.

Episode 59 handles that tension well. Instead of pretending the economy can be explained by one neat signal, it leans into a more realistic truth: the economy is hard to understand because it is full of conflicting data, lagging indicators, sentiment swings, policy decisions, and human behavior. A strong labor market can coexist with falling risk appetite. Corporate profits can look decent while investors act like the sky has filed for divorce. The market is a forward-looking machine, but it is run by people who still overreact to last week’s headlines.

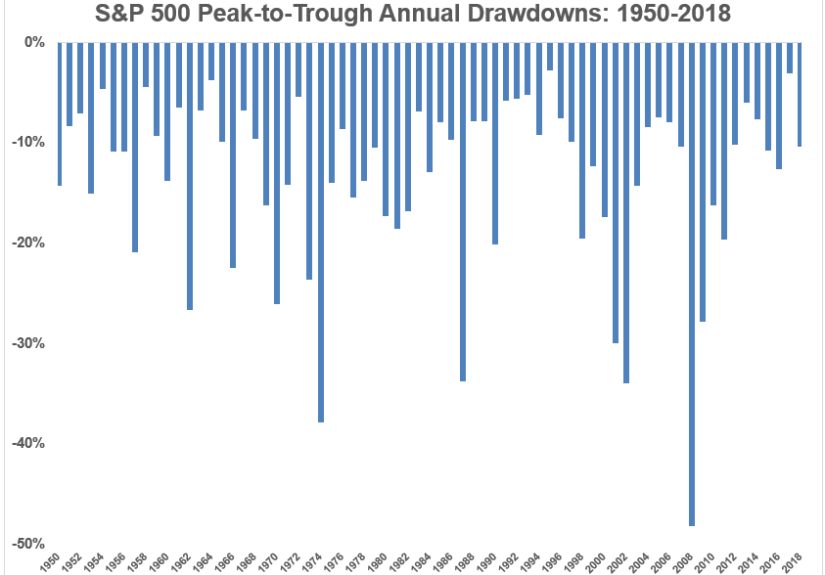

Why Every Market Correction Feels Different

One of the best themes in this episode is also one of the most durable: every correction feels unique while you are living through it. That is true even when the basic mechanics are familiar. Prices fall. Confidence drops. Financial television rediscovers the concept of fear. People who ignored risk for months suddenly develop a passionate interest in capital preservation. And somewhere, someone says, “This time is different,” which is often financial history’s version of stepping on a rake.

The genius of this observation is that it respects both facts at once. Yes, each drawdown has its own trigger. One correction may revolve around inflation scares. Another may center on the Fed. Another may come from credit stress, geopolitics, an overvalued tech trade, or a plain old growth scare. But emotionally, corrections rhyme. They create discomfort, and discomfort convinces investors that the current pain must be more meaningful than previous pain.

That mental trap matters because it nudges people toward bad decisions. When stocks slide, investors stop asking, “What is my time horizon?” and start asking, “How do I make this feeling go away by lunch?” The market, meanwhile, remains rude enough to recover on its own schedule.

Late 2018 was a perfect setup for this kind of anxiety. The expansion was old. Rate hikes were in the conversation. Risk assets had lost their easy swagger. Suddenly, “normal volatility” felt like a profound moral emergency. Episode 59 pushes back on that instinct by reminding listeners that market losses, even uncomfortable ones, are often part of the deal. If you want long-term equity returns without drawdowns, you are basically asking for a roller coaster that is all souvenir photo and no drop.

The Market’s Favorite Magic Trick

The market loves to turn normal into dramatic. A correction that fits historical patterns can still feel shocking in real time because investors do not experience volatility as a statistic. They experience it as a blinking red number attached to their retirement account, college fund, or ego. That is why even seasoned investors can know the history and still react like they just saw a ghost in the pantry.

Episode 59 is especially sharp here because it never treats emotional reactions as stupidity. Fear is not irrational simply because markets have fallen before. Fear is human. The mistake is letting fear become strategy.

Why a Shallow Recession and a Plain-Vanilla Bear Market Can Be Healthy

This was one of the more interesting ideas tied to the episode: the notion that a shallow recession and a run-of-the-mill bear market might actually be preferable to the alternatives. That sounds strange until you think about what the alternatives are. If excesses build for too long, imbalances can get bigger, leverage can creep higher, and valuations can become more fragile. Small resets are rarely fun, but they can be healthier than waiting for a giant blowout that turns a routine slowdown into a systemic mess.

In other words, there is a difference between a market cleaning its room and a market setting the house on fire. Investors often wish for no pain at all, but cycles do not work that way. A mild downturn can cool off excess speculation, force better discipline, and reset expectations without destroying the whole financial plumbing system.

That idea also reveals a mature investing mindset. Not every decline is a tragedy. Some declines are the price of keeping the broader system from getting too weird. Nobody enjoys the medicine, but it is usually better than pretending the fever is a personality quirk.

The Economy Is Hard to Read Because It Sends Mixed Signals

Late-cycle environments are confusing because the economy often looks strongest right before it weakens. Unemployment can be low. Consumers may still be spending. Businesses might still be hiring. Yet under the surface, the yield curve flattens, financing conditions tighten, and markets begin sniffing out slower growth ahead. Investors are left trying to reconcile a healthy present with a nervous future.

That is one reason the episode’s title works so well. “Late cycle” is not just an economic label. It is a psychological condition. It is the point in an expansion when good news stops feeling reassuring and starts feeling temporary. Strong jobs data? Nice, but maybe too strong for inflation. Healthy spending? Great, unless it keeps rates higher. Solid corporate earnings? Wonderful, unless margins are peaking. In late cycle, almost every positive data point arrives with a suspicious side-eye.

This is why simple storytelling breaks down. Investors desperately want a single indicator that explains everything. But markets are not vending machines. You cannot insert one data point and receive one certain future. Episode 59 understands that reality. It treats the economy as messy, layered, and resistant to neat answers, which is exactly how it behaves when money is involved.

The Alpha Fantasy: Why Smart Institutions Still Think They’re Special

Another standout theme in this episode is the enduring belief that sophisticated investors can find alpha even when the evidence keeps giving them side-eye. Institutional investors, consultants, and professional allocators often talk as though manager selection is a secret passageway to better outcomes. Sometimes it works. Often it becomes a very expensive way to discover that humility was the cheaper option all along.

This is not an argument that active management never works. Exceptional managers exist. Skilled security selection exists. But the broader lesson is that the industry routinely overestimates how easy it is to identify skill ahead of time, stick with it through inevitable underperformance, and avoid paying too much for the privilege.

That is what makes the alpha discussion in Late Cycle feel so relevant. When markets are calm, investors love complexity because complexity feels premium. In shakier periods, complexity starts to look suspiciously like a fee schedule wearing a tuxedo. The fantasy is not just that alpha exists. The fantasy is that it can be reliably spotted, hired, and harvested without being diluted by costs, crowding, turnover, or plain old bad timing.

Late cycle tends to intensify that urge. As returns get harder to come by, investors become more vulnerable to the sales pitch that someone, somewhere, has a clever process, a smarter model, or a genius with excellent cheekbones who can thread the needle. Sometimes the better answer is duller: diversify, keep costs low, rebalance when appropriate, and stop acting like every market phase requires a costume change.

Why the Passive Debate Keeps Coming Back

The passive-versus-active debate never really ends because it is not just a portfolio issue. It is a self-image issue. Passive investing asks people to accept that the market may be hard to beat consistently. For many professionals, that is emotionally offensive. It is much more comfortable to believe that complexity signals intelligence and that intelligence should be monetized at two percent plus feelings.

Episode 59 captures that tension without turning it into a cartoon. The point is not that everyone should invest the same way. The point is that investors should be honest about the odds, the costs, and the role of ego in manager selection.

Money, Happiness, and the Lottery Problem

One reason this episode feels more human than many market recaps is that it wanders into the question of whether rich people are actually happier and whether winning the lottery would really improve life. That may sound like a detour, but it is not. It is a behavioral-finance mirror.

Markets are full of people chasing more: more returns, more status, more optionality, more proof that they were right. But the relationship between money and happiness is not linear in the way ambition likes to imagine. Money absolutely matters. It can reduce stress, increase security, expand choices, and improve life satisfaction. At the same time, comparison, adaptation, and expectation can make additional wealth less emotionally transformative than people assume.

The lottery angle is especially useful because it pokes at one of the oldest fantasies in finance: the idea that one giant win solves the human condition. In reality, windfalls can improve financial satisfaction while leaving the deeper machinery of happiness far more complicated. People adapt. They compare themselves to new peers. Yesterday’s miracle becomes today’s baseline. The champagne goes flat; the taxes do not.

This part of the episode broadens the conversation in a smart way. Markets are not just about capital allocation. They are also about the stories people tell themselves regarding what money will do for them. Episode 59 quietly asks an uncomfortable question: if your portfolio grows and you are still restless, what exactly were you investing for?

The Practical Lessons From Animal Spirits Episode 59

If you strip away the headlines, the cycle talk, and the side quests into money psychology, the episode leaves investors with a pretty practical playbook.

- Do not confuse late cycle with immediate collapse. Expansions usually cool before they crack, and that cooling period can last longer than impatient investors expect.

- Treat corrections as part of investing, not proof that investing is broken. Volatility is not a software bug. It is the subscription fee.

- Respect history without pretending it predicts the calendar. Cycles rhyme, but they do not send invitations.

- Be skeptical of alpha theater. The line between skill and storytelling gets blurry when returns get harder to find.

- Remember that money solves some problems, not all of them. Wealth can help enormously, but it does not automatically produce peace, meaning, or perspective.

In a way, that is the enduring charm of this episode. It does not promise certainty. It teaches temperament. And temperament, unlike the hot take of the week, tends to stay useful.

Experiences From Living Through a Late-Cycle Market

If you have ever invested through a late-cycle stretch, you know the feeling is weirdly specific. It is not the pure optimism of an early recovery, when everything looks cheap and every bounce feels deserved. It is not the full despair of an actual recession either, when the damage is obvious and the headlines stop pretending. Late cycle feels like walking through an airport with a delayed flight: technically everything is still operating, but nobody is relaxed and every announcement sounds vaguely threatening.

You start noticing how investor behavior changes in small ways. Friends who never asked about the Fed suddenly ask whether one more rate hike will “break something.” People who spent the previous year bragging about aggressive growth stocks start saying they have “always believed in quality.” Cash, which recently looked boring, now gets discussed like it is a spiritual practice. Everyone becomes very interested in downside protection right after discovering that downside exists.

There is also a special kind of mental fatigue that arrives late in the cycle. Good news no longer feels purely good. A strong jobs report can sound inflationary. A soft inflation print can sound recessionary if it is too soft. Strong earnings might suggest resilience, but they can also trigger arguments that margins have peaked. Every data release becomes a Rorschach test for anxious people with brokerage apps. The market is not just moving; it is mood-swinging in public.

For long-term investors, that phase can be oddly educational. You learn that conviction is easy when your account goes up in a straight line and much harder when your carefully built portfolio starts looking like it made several regrettable life choices. You learn that diversification is comforting in theory and occasionally annoying in practice. You learn that the people shouting the loudest on social media are often selling emotion, not insight.

Most importantly, you learn that late-cycle investing is less about predicting the exact turn and more about managing yourself while the turn is still uncertain. That may mean rebalancing instead of panicking. It may mean reviewing your time horizon instead of doomscrolling. It may mean accepting that some drawdowns are not signs that your plan failed; they are signs that your plan is being tested in the wild, where markets are noisy, rude, and unimpressed by your need for reassurance.

There is also a strange gift hidden in late-cycle periods: they expose what you actually believe. If you say you are a long-term investor, a bumpy market will ask for evidence. If you say you can tolerate risk, a correction will request documentation. If you claim you do not care what everyone else is doing, a few ugly weeks will reveal whether that was philosophy or just excellent weather. Late cycle has a way of stripping off the branding and leaving the investor.

That is why Animal Spirits Episode 59: Late Cycle still resonates. It captures more than a market moment. It captures the lived experience of being an investor when confidence is fading but the story is not finished. The episode understands that late cycle is not merely an economic phase. It is a test of patience, humility, and emotional range. And for many investors, that test turns out to be far more important than guessing the exact date when the next recession finally puts its shoes on.

Conclusion

Animal Spirits Episode 59: Late Cycle works because it refuses to flatten investing into a single headline. It acknowledges that markets get messy, that cycles mature, that corrections feel personal, and that humans remain gloriously bad at separating money from emotion. The episode is about late-cycle investing, yes, but it is also about perspective. That is the real advantage it offers listeners.

The smartest takeaway is not a tactical trade. It is a mental reset. Late cycle does not demand a panic button. It demands realism. Markets can wobble without ending. Economies can slow without collapsing. Active-management dreams can survive long after the evidence gets awkward. And money can improve life without solving the entire puzzle of happiness.

In other words, this episode is less about calling the top and more about keeping your head when everyone around you starts acting like the closing bell is an evacuation siren. In finance, that is not just good podcasting. That is survival skill.