Table of Contents >> Show >> Hide

- What Does “Locking in 5% Yields” Actually Mean?

- Why 5% Yields Feel So Tempting

- Where Investors May Still Find Yields Near 5%

- When Locking in a Yield Makes Sense

- When Locking in 5% Yields Could Be a Mistake

- CDs vs. Treasuries vs. Money Market Funds

- The Role of Interest Rate Risk

- Taxes Can Change the Winner

- How Much Should You Lock In?

- Practical Experiences Related to Locking in 5% Yields

- Final Verdict: Is It Time To Lock in 5% Yields?

- SEO Tags

For years, savers were treated like the financial world’s houseplants: expected to sit quietly in the corner and survive on almost no nourishment. Then rates jumped, cash started paying real income again, and suddenly a plain old certificate of deposit looked less like grandma’s dusty banking tool and more like a tiny income machine wearing sensible shoes.

Now investors are asking a very reasonable question: Is it time to lock in 5% yields? The answer is not a dramatic “yes” or “no.” It is more like: yes for some money, maybe for some goals, and absolutely not for money that needs growth, flexibility, or protection from inflation over many years.

As of early May 2026, true 5% yields are not everywhere. The Federal Reserve’s policy rate is lower than the peak of the recent cycle, Treasury yields have settled below 5% across many maturities, and many high-quality CDs are closer to the low-4% range. Still, occasional promotional CDs, short-term bank specials, and certain income investments may offer headline yields near 5%. That makes this a great moment to understand what “locking in” really means before your money signs a long-term lease.

What Does “Locking in 5% Yields” Actually Mean?

To lock in a yield means you buy a fixed-income product that promises a stated return if you hold it under the required terms. A traditional CD may pay a fixed annual percentage yield for six months, one year, three years, or five years. A Treasury note or individual bond may offer a yield to maturity that you can expect if you hold until maturity and the issuer pays as promised.

That is different from leaving money in a high-yield savings account or money market fund. Those products can be attractive, but their yields float. When the Federal Reserve cuts rates or market conditions change, your rate can quietly shrink while you are making coffee. No breakup text, no apology, just a lower yield.

Fixed Yield vs. Floating Yield

A fixed yield is useful when you want predictability. A floating yield is useful when you want flexibility. The best choice depends on the job of the money. Emergency savings usually needs liquidity. A down payment needed in nine months may value safety and timing. Retirement income may need a laddered approach. Long-term wealth building usually needs more than cash-like returns.

Why 5% Yields Feel So Tempting

A 5% yield has a nice psychological ring to it. It sounds clean, sturdy, and respectable, like a financial handshake from someone who owns a label maker. On $100,000, a 5% annual yield means roughly $5,000 in income before taxes. That is meaningful money, especially for retirees, conservative investors, or anyone tired of watching idle cash do absolutely nothing.

The appeal becomes even stronger after years of near-zero savings rates. Many investors remember when bank accounts paid almost nothing and “cash management” basically meant choosing which account would disappoint you slightly less. Compared with that era, a 4% to 5% yield feels luxurious.

The Real Return Question

However, the number that matters is not just the stated yield. It is the after-tax, after-inflation return. If inflation runs near 3% and your CD pays 5%, your rough real return before taxes is about 2%. After taxes, the advantage may be smaller. That does not make the yield bad. It simply means the return is not magic. It is income, not a free money fountain guarded by a friendly dragon.

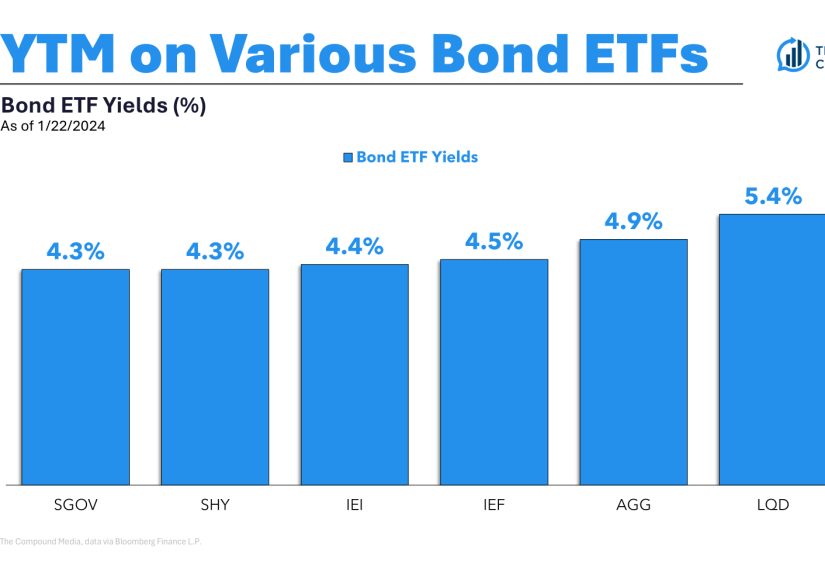

Where Investors May Still Find Yields Near 5%

In the current market, 5% yields are more selective than they were when short-term rates were at their recent highs. The best advertised CD rates may occasionally reach 5%, but they are often promotional, short-term, deposit-limited, or offered by specific credit unions with membership rules. Many widely available top CD rates are closer to 4% to 4.25%, while national averages are much lower.

Certificates of Deposit

CDs are one of the simplest ways to lock in a rate. You deposit money for a set term, the bank or credit union pays interest, and you generally receive your principal back at maturity. CDs from FDIC-insured banks or NCUA-insured credit unions can be very safe when balances stay within insurance limits.

The trade-off is liquidity. If you withdraw early from a bank CD, you may pay an early withdrawal penalty. Brokered CDs can sometimes be sold before maturity, but their market value may rise or fall depending on interest rates. In plain English: a CD is simple, but not always as flexible as it looks in the brochure.

Treasury Bills and Notes

U.S. Treasury bills are short-term government securities issued with maturities from four weeks to 52 weeks. They are sold at a discount or at par, and investors receive the face value at maturity. Treasuries are backed by the full faith and credit of the U.S. government, which makes them a core option for conservative investors.

Treasury yields may not always match the highest CD specials, but they have a tax advantage: Treasury interest is generally exempt from state and local income taxes. For investors in high-tax states, that can make a slightly lower Treasury yield competitive with a higher bank yield.

Money Market Funds

Money market funds can be useful for liquidity and short-term parking. They typically invest in high-quality, short-term securities and quote a seven-day SEC yield. Their rates can adjust quickly as the interest rate environment changes.

But money market funds are not bank deposits and are not FDIC insured. They are generally designed to be stable, but they still carry investment risk. Think of them as convenient cash tools, not guaranteed bank accounts wearing a mutual fund costume.

High-Quality Bonds

Investment-grade corporate bonds, municipal bonds, and bond funds may offer attractive yields, but they bring different risks. Corporate bonds add credit risk. Municipal bonds add tax and issuer-specific considerations. Bond funds can lose value when rates rise, especially if they hold longer-duration securities.

That does not make bonds bad. It means investors should know whether they are buying guaranteed principal at maturity from an individual bond, market exposure through a fund, or a mix of both. The yield is only one chapter of the story.

When Locking in a Yield Makes Sense

Locking in a yield can be smart when the money has a known purpose and a known time frame. For example, if you need $30,000 for a home renovation in 12 months, a 12-month CD or Treasury bill may be a reasonable fit. You are not trying to beat the stock market. You are trying to keep the money safe, earn income, and avoid accidentally spending it on “just one more” online cart.

Good Candidates for Locked-In Yields

Locking in may make sense for emergency fund overflow, near-term goals, conservative retirement income, college money needed soon, or cash that is currently earning little. It can also help investors who worry that short-term rates will fall and want to preserve today’s income for a little longer.

A CD or Treasury ladder can be especially useful. Instead of putting all your cash into one maturity, you divide it across several maturities. For example, you might place money into 6-month, 12-month, 18-month, and 24-month instruments. As each rung matures, you can spend it, reinvest it, or adjust based on current rates.

When Locking in 5% Yields Could Be a Mistake

A guaranteed yield can feel safe, but safety depends on the goal. If you are investing for 20 or 30 years, locking too much money into cash-like products may create opportunity cost. Stocks are volatile, but historically they have offered higher long-term return potential than cash and short-term fixed income. A 5% CD can be excellent for a one-year goal and underpowered for a 30-year retirement plan.

Beware of Chasing the Headline Number

Some products advertise high yields because they carry more risk. A 5% CD insured by a bank is not the same as a 5% high-yield bond fund, a preferred stock, a real estate investment trust, or a dividend stock. The income may look similar. The risk can be completely different.

Investors should ask three questions before chasing any yield: Is the principal protected? Can the income change? What must happen for me to receive the advertised return? If the answer is hard to understand, that is not sophistication. That is a warning label wearing a necktie.

CDs vs. Treasuries vs. Money Market Funds

Choosing between CDs, Treasuries, and money market funds is mostly about trade-offs. CDs can offer strong rates and deposit insurance, but they may penalize early withdrawals. Treasuries offer strong credit quality and state-tax advantages, but their market value can fluctuate if sold before maturity. Money market funds offer liquidity, but yields are variable and not FDIC insured.

A Simple Example

Suppose an investor has $60,000 set aside for a home purchase in 18 months. Putting all of it into a five-year CD would be awkward because the timing does not match the goal. Leaving all of it in a savings account may be flexible but could expose the investor to falling rates. A more balanced approach might be a ladder of Treasury bills or CDs maturing around the expected purchase date.

Now suppose a retiree wants predictable income from part of a portfolio. A ladder of CDs, Treasuries, or high-quality bonds could help create cash flow without selling stocks during market downturns. The ladder does not eliminate risk, but it makes the plan easier to manage.

The Role of Interest Rate Risk

Interest rate risk is the see-saw of fixed income. When market rates rise, the price of existing bonds usually falls. When market rates fall, existing bonds with higher coupons can become more valuable. This matters most if you sell before maturity or own bond funds.

For CDs and individual Treasuries held to maturity, price fluctuations may matter less because the plan is to receive principal back at maturity. But if you buy a long-term bond and need cash early, market prices can matter a lot. Longer maturities usually bring more sensitivity to rate changes.

Reinvestment Risk Is the Other Side

Reinvestment risk means your current high-yielding investment matures and you cannot find a similar rate. This is the main argument for locking in rates today. If you keep everything in a floating-rate account and yields fall, your income falls too. A ladder can reduce this risk without forcing you to make one all-or-nothing bet.

Taxes Can Change the Winner

Taxes are where yield comparisons get sneaky. A 5% bank CD may look better than a 4.6% Treasury at first glance. But Treasury interest is generally free from state and local income tax, while CD interest is usually taxable at federal, state, and local levels. For investors in high-tax states, the after-tax Treasury yield may be more competitive than the headline number suggests.

Municipal bonds add another layer. Their yields may look lower, but the interest may be federally tax-exempt and sometimes state-tax-exempt if issued by the investor’s home state. Munis are not automatically better, but for higher-income investors, the tax-equivalent yield can be worth calculating.

How Much Should You Lock In?

The right amount depends on your goals, timeline, tax situation, and risk tolerance. A practical framework is to sort money into buckets. The first bucket is emergency cash, which should remain liquid. The second bucket is money needed within one to three years, where CDs, Treasuries, and high-yield savings may fit. The third bucket is long-term money, where growth assets may still deserve a major role.

A Balanced Strategy

Instead of asking, “Should I lock in 5% yields?” ask, “Which dollars need certainty?” That question is much better. It keeps investors from locking up too much cash just because a rate looks attractive. It also prevents the opposite mistake: leaving every dollar floating when some predictable income would be useful.

Practical Experiences Related to Locking in 5% Yields

The experience of locking in a high yield is often less glamorous than people expect, but that is part of the charm. You do not get fireworks. You get a confirmation page, a maturity date, and the oddly satisfying feeling that a portion of your money now has a job description.

One common experience is the relief of moving idle cash into something structured. Many savers discover that they have been keeping far more than necessary in a checking account earning close to nothing. Once they shift part of that money into a CD, Treasury bill, or money market option, they start seeing monthly or maturity-based income. It is not life-changing overnight, but it feels like finally putting lazy dollars on a treadmill.

Another experience is learning that the highest advertised yield is not always the best choice. A 5% CD may come with a short term, a low deposit cap, strict membership rules, or an early withdrawal penalty. A slightly lower-yielding Treasury may be easier to buy, simpler to ladder, and better after taxes for some investors. People often begin by chasing the biggest number and end by appreciating the best fit.

There is also the emotional benefit of predictability. Investors who lived through volatile stock markets often enjoy knowing that a portion of their portfolio is scheduled to mature on a specific date. This can be especially helpful for retirees who need regular cash flow. A ladder can create a rhythm: one security matures, cash becomes available, and the investor decides whether to spend or reinvest. It turns financial planning from a guessing game into a calendar.

But the experience is not perfect. Some investors feel regret if they lock in a rate and then rates rise. Others feel annoyed when they lock in a short-term CD and, six months later, the renewal rate is lower. That is why laddering can be more comfortable than making one big decision. It spreads the timing risk and reduces the emotional drama. Financial decisions are easier when they do not require psychic powers.

Another lesson is that liquidity matters more than expected. A household may think it can lock up cash for two years, only to face a car repair, tuition bill, medical expense, or job change. This is why emergency funds should not be sacrificed for a slightly higher yield. A 5% return is nice. Being able to access money when life throws a wrench through the window is nicer.

Finally, many investors realize that locked-in yields are a tool, not a full financial plan. They can protect short-term money, support income needs, and reduce reinvestment risk. They cannot replace long-term growth, erase inflation, or guarantee that every future decision will feel perfect. Used well, they add stability. Used carelessly, they can create opportunity cost or liquidity headaches.

Final Verdict: Is It Time To Lock in 5% Yields?

For money that needs safety, timing, and predictable income, yes, it may be a good time to lock in attractive yields while they are still available. But investors should be realistic: true 5% opportunities are more limited than they were, and many high-quality options now sit closer to 4% than 5%.

The smartest approach is not to chase the biggest headline APY. It is to match the investment to the purpose. Use liquid accounts for emergency funds. Consider CDs or Treasuries for short-term goals. Build ladders when timing is uncertain. Keep long-term money invested according to a broader plan. And always compare after-tax returns, not just shiny numbers.

In other words, locking in 5% yields can be a smart move for the right dollars. Just do not let a good yield talk you into a bad fit. Money should work hard, but it should also be available when you need it. Even the best yield is not worth turning your financial life into a locked drawer with a missing key.