Table of Contents >> Show >> Hide

- What Is a Market Correction, Exactly?

- What “Winning” During a Correction Really Means

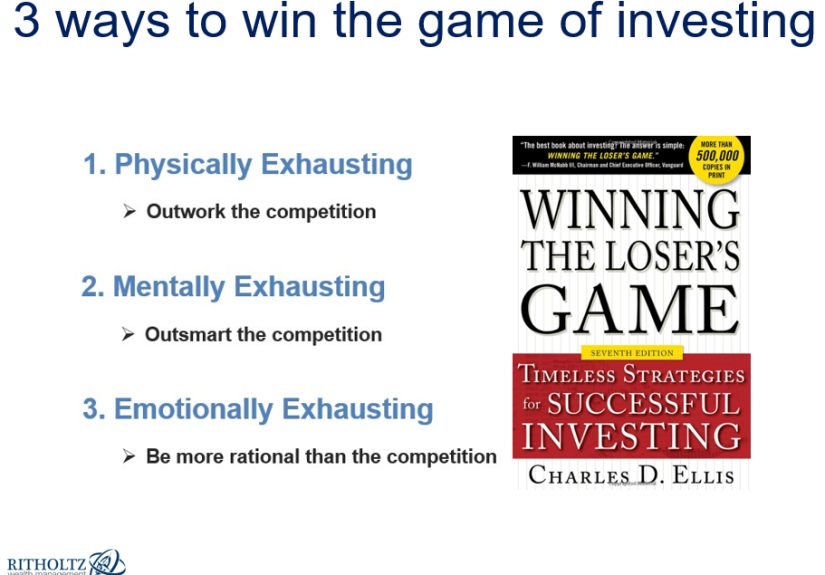

- The 3 Ways to Win During a Market Correction

- A Quick Correction Action Plan (So You Don’t Panic at 2:13 a.m.)

- Common Mistakes to Avoid During a Market Correction

- Final Takeaway

- Added Experience Section (Approx. ): What This Looks Like in Real Life

Educational content only. Not personalized financial, investment, or tax advice.

If the words market correction make you want to hide under a blanket with your brokerage app turned upside down, you are not alone. Corrections are uncomfortable by design. They show up fast, make headlines louder, and convince otherwise rational adults that checking their portfolio 17 times before lunch is somehow a strategy.

But here’s the good news: a correction does not automatically mean disaster. In many cases, it’s a normal part of investing. And if you handle it with a plan instead of panic, a correction can become a moment where you actually improve your long-term results.

This guide breaks down the 3 ways to win during a market correctionwithout pretending you can predict the exact bottom (because no one has a crystal ball, and if they do, they’re definitely not posting it for free).

What Is a Market Correction, Exactly?

A market correction is generally defined as a decline of about 10% to less than 20% from a recent market high. Once a decline reaches 20% or more, many people start calling it a bear market. That distinction matters because it helps investors avoid mixing up a painful-but-common pullback with a deeper, longer downturn.

Corrections can be triggered by many things: changing interest-rate expectations, economic slowdown fears, policy uncertainty, earnings disappointments, or just a market that sprinted too far, too fast and needs a breather. In other words, markets sometimes correct the way your back does after moving furniture all weekendunpleasant, but not always a sign of permanent damage.

The key mindset shift is this: volatility is part of the price of admission for long-term investing. If you want growth assets, you also need a plan for the periods when they wobble.

What “Winning” During a Correction Really Means

Winning during a correction does not mean perfectly buying the bottom, making a dramatic all-in move, and telling your friends you “saw it coming.” In real life, winning usually looks like this:

- You avoid panic-selling and locking in losses.

- You keep your portfolio aligned with your goals and risk tolerance.

- You continue investing (or deploy cash) with discipline.

- You use the downturn to improve tax efficiency and portfolio quality.

- You come out of the correction with a stronger process than before.

That may sound less exciting than “turn $5,000 into a yacht,” but it’s a much better recipe for long-term wealth building.

The 3 Ways to Win During a Market Correction

1) Win by Controlling Behavior and Rebalancing (Not Reacting)

The first and biggest win is behavioral: don’t let a temporary drawdown turn into a permanent mistake. Many investors do the most damage not during the correction itself, but in the decisions they make while stressedselling after a drop, waiting for “clarity,” and then missing part of the rebound.

That’s why your first move should be to return to your investment plan and ask:

- Has my time horizon changed?

- Has my risk tolerance truly changed?

- Do I need this money soon?

- Or am I just uncomfortable because the screen is red?

If your goals and timeline are the same, a correction often calls for rebalancing, not reinventing your entire portfolio. Rebalancing means bringing your asset mix back to your target allocation. For example, if stocks fell and now your portfolio is lighter on equities than planned, you may rebalance by adding to stocks (or directing new contributions there) so your risk level matches your original plan.

That sounds simple. Emotionally, it feels like eating vegetables at a birthday party. Rebalancing often asks you to buy what recently underperformed and trim what held up better. But that “buy lower, trim higher” discipline is exactly why it works over time.

How to do it in practice:

- Set a rule: Rebalance on a schedule (quarterly/semiannually) or when allocations drift by a certain percentage.

- Use contributions first: If possible, direct new money to underweight asset classes before selling anything.

- Keep taxes and fees in mind: Rebalancing in tax-advantaged accounts may reduce tax friction.

- Write down your plan: Decisions made in calm times are usually better than decisions made after a scary headline.

Behavioral win = you stay in the game. Rebalancing win = you stay aligned with your strategy.

2) Win by Investing Consistently (Dollar-Cost Averaging Beats Guessing)

The second way to win is to turn uncertainty into a system: keep buying on a schedule.

This is where dollar-cost averaging (DCA) shines. DCA means investing a fixed dollar amount at regular intervals regardless of whether the market is up, down, or doing its usual dramatic monologue. When prices fall, your set amount buys more shares. When prices rise, it buys fewer. Over time, this can reduce the emotional pressure of trying to “time the perfect entry.”

Here’s a simple example:

Let’s say you invest $1,000 per month into a broad index fund during a correction. In month one, the fund is $100/share (you buy 10 shares). In month two, it drops to $80/share (you buy 12.5 shares). In month three, it drops to $75/share (you buy 13.33 shares). If markets later recover, those lower-priced purchases can do a lot of heavy lifting.

DCA is especially useful for:

- 401(k) and retirement plan contributions

- Monthly IRA investing

- People who are nervous about investing a lump sum

- Investors building a position gradually during volatility

Important reality check: DCA is a discipline tool, not a magic trick. It does not prevent losses, and in some market environments lump-sum investing may outperform. But if DCA helps you stay consistent instead of staying frozen in cash, it can be a very effective strategy during a correction.

How to make DCA work better:

- Automate it so emotions don’t get a vote every week.

- Use diversified investments (e.g., broad funds) unless you have a strong thesis and risk tolerance for individual stocks.

- Pair DCA with a long-term target allocation so your buying supports an actual plan.

- Avoid doom-scrolling before each contribution date. (Your future self thanks you.)

Consistency is boringand in investing, boring is often beautiful.

3) Win by Upgrading Your Portfolio and Tax Strategy While Prices Are on Sale

The third way to win during a market correction is to use it as a portfolio-improvement window. When prices fall, investors who are calm and organized can make smart upgrades they might ignore during bull markets.

A. Improve portfolio quality and diversification

Corrections are a good time to ask hard questions:

- Am I overconcentrated in one stock, sector, or theme?

- Do I actually have diversification, or just 12 versions of the same trade?

- Does my asset allocation match my age, goals, and risk tolerance?

- Do I have enough liquidity for near-term expenses?

Sometimes “winning” means buying quality assets at better prices. Other times it means reducing concentration risk and building a more resilient mix of stocks, bonds, and cash. A correction can reveal portfolio weak spots the same way a rainstorm reveals which window actually leaks.

If you’re still accumulating wealth, adding to diversified long-term holdings during a correction may strengthen future return potential. If you’re closer to a goal (retirement, tuition, home purchase), winning may look more like risk management and making sure your short-term money is not exposed to stock market swings.

B. Consider tax-loss harvesting (carefully)

In taxable accounts, a correction may create opportunities for tax-loss harvestingselling an investment at a loss to potentially offset capital gains (and in some cases reduce taxable income, subject to tax rules and limits). This can improve after-tax returns over time.

But there’s a major trap: the wash-sale rule. If you sell a holding for a loss and buy the same (or substantially identical) security within the restricted window around that sale, the loss may be disallowed for current tax deduction purposes. That means you need a thoughtful replacement strategy, good records, andideallyhelp from a tax professional if your situation is complex.

Smart tax-loss harvesting habits:

- Only harvest in taxable accounts (not retirement accounts) unless you clearly understand the implications.

- Know your replacement plan before you sell.

- Avoid accidental repurchases through automatic dividend reinvestment or spouse accounts.

- Focus on long-term tax efficiency, not short-term tax “wins” that distort your portfolio.

A correction is one of the few times the market may hand you a tax planning opportunity and a portfolio cleanup opportunity at the same time. Don’t waste it by winging it.

A Quick Correction Action Plan (So You Don’t Panic at 2:13 a.m.)

- Pause before acting. A correction is not an emergency by default.

- Review your time horizon and cash needs. Near-term money should not be taking long-term stock risk.

- Check allocation drift. Rebalance if needed according to your rules.

- Keep contributions going. Automate DCA wherever possible.

- Evaluate tax-loss harvesting in taxable accounts. Respect wash-sale rules.

- Reduce noise. Fewer headlines, more process.

- Document your playbook. Future you will need it in the next correction too.

Common Mistakes to Avoid During a Market Correction

- Going all to cash without a plan: This can turn a temporary drawdown into a long-term setback.

- Trying to call the exact bottom: Even professionals miss it regularly.

- Confusing a good company with a good portfolio weight: Concentration risk is real.

- Ignoring taxes when rebalancing: What looks clean on paper may create an avoidable tax bill.

- Treating social media as a fiduciary: “Trust me bro” is not an investment policy statement.

Final Takeaway

The 3 ways to win during a market correction are simple to say and hard to do:

- Control behavior and rebalance instead of reacting.

- Invest consistently through volatility with dollar-cost averaging.

- Use the downturn to improve diversification, portfolio quality, and tax efficiency.

Notice what’s missing from that list: predicting headlines, guessing the bottom, and becoming an overnight macroeconomist because you watched two videos. Corrections reward discipline more than drama. If you build a repeatable process now, the next market wobble may still be uncomfortablebut it won’t be chaos.

That’s a real win.

Added Experience Section (Approx. ): What This Looks Like in Real Life

One of the most useful lessons about market corrections comes from seeing how different investors behave when the pressure is on. The patterns are surprisingly consistent.

Experience #1: The Panic Seller. A common story goes like this: an investor watches a portfolio drop 8%, then 12%, then 15%. Headlines get worse. Friends start saying, “I moved everything to cash until things settle down.” The investor sells, feels immediate relief, and tells themselves they’ll get back in soon. But “soon” turns into weeks, then months, because the market rebounds before the news feels safe again. The biggest pain wasn’t the correctionit was missing the recovery. The lesson: emotional relief and good investing decisions are not always the same thing.

Experience #2: The Automatic Investor. Another investor barely looks at daily headlines because their retirement contributions and monthly brokerage deposits are automated. During the correction, they keep buying. It doesn’t feel heroic. In fact, it feels almost anticlimactic. But later, when markets recover, those purchases made at lower prices improve the long-term average cost of their holdings. The lesson: systems beat willpower. Automation can protect you from your own short-term emotions.

Experience #3: The Overconcentrated “Winner.” This investor had great returns before the correction because one sector or one stock became a huge percentage of the portfolio. Then the correction hits that exact area hardest. Suddenly, what looked like genius starts looking fragile. The investor realizes they were diversified by ticker symbol, not by actual risk exposure. During the correction, they rebalance and spread risk more intentionally. The lesson: a correction can be an expensive teacher, but it can also be a timely one.

Experience #4: The Tax-Aware Planner. Some investors use corrections to review taxable accounts, harvest losses where appropriate, and swap into similar (not substantially identical) investments to maintain exposure. They don’t chase tax moves blindly, and they document everything. By the end of the year, they may have improved their tax position without abandoning their long-term allocation. The lesson: downturns can create opportunities for organized investors, especially when tax strategy is part of the plan.

Experience #5: The “Now I Need a Plan” Moment. Many people only discover their true risk tolerance during a correction. A portfolio that felt fine in an up market suddenly feels too aggressive when volatility shows up. That realization isn’t failureit’s useful information. Some investors respond by building a written allocation policy, setting rebalancing thresholds, and separating emergency savings from investment assets. The lesson: the best time to create a correction playbook was before the sell-off; the second-best time is right now.

Across all these experiences, the takeaway is the same: market corrections expose habits. If your habit is panic, corrections feel like punishment. If your habit is process, corrections can become progress.