Table of Contents >> Show >> Hide

- Why the 50-Year Mortgage Keeps Coming Back

- The Core Economic Tradeoff: Smaller Payment, Much Bigger Lifetime Cost

- Equity Growth: The Hidden Cost Nobody Brags About

- Why 50-Year Mortgages Are a Bad Fit for the U.S. Mortgage System

- Would a 50-Year Mortgage Actually Improve Housing Affordability?

- Who Might Actually Benefit?

- Smarter Alternatives to a 50-Year Mortgage

- The Bottom Line

- Real-World Experiences With the Economics of a 50 Year Mortgage

On paper, a 50-year mortgage sounds like the sort of thing that should arrive wearing a cape. Lower monthly payments? Easier homeownership? A rescue plan for buyers who look at today’s housing market and laugh so they do not cry? It is an appealing pitch. In an era when housing affordability has been squeezed by elevated mortgage rates, high home prices, and a stubborn housing shortage, stretching the loan term feels like a clever hack.

But the economics of a 50-year mortgage are not magic. They are math. And mortgage math is a ruthless little goblin. A longer loan term can absolutely reduce the monthly principal-and-interest payment, but it also keeps borrowers in debt longer, slows equity growth, and can dramatically increase total interest costs. In the United States, where the mainstream mortgage market is built around 15-year and 30-year loans, a 50-year mortgage would not just be unusual. It would also collide with pricing, regulation, investor appetite, and the simple fact that lower payments do not automatically create cheaper housing.

This is why the economics of a 50-year mortgage deserve more than a quick “sounds nice” reaction. The real question is not whether the payment is smaller. The real question is whether the tradeoff is worth it.

Why the 50-Year Mortgage Keeps Coming Back

The idea resurfaces whenever affordability gets ugly. And affordability has been ugly. Recent U.S. housing research shows that even after some improvement, the median borrower putting 3.5% down was still spending about 34% of income on a mortgage by late 2025. That is above the classic 30% affordability rule of thumb. Meanwhile, Freddie Mac has estimated the U.S. housing market remains undersupplied by millions of homes, which means the problem is not just financing. It is also supply. When there are not enough homes, buyers do not need a miracle; they need either more income, lower rates, lower prices, or more homes to choose from.

Still, longer loan terms are tempting because they attack the most visible pain point: the monthly payment. Consumers do not experience homeownership as a spreadsheet first. They experience it as a payment due every month, with taxes, insurance, repairs, and the occasional soul-crushing HVAC surprise attached. If a 50-year mortgage lowers the payment enough to make a deal fit a household budget, it is easy to see why the idea gets traction.

That is the emotional case. The financial case is more complicated.

The Core Economic Tradeoff: Smaller Payment, Much Bigger Lifetime Cost

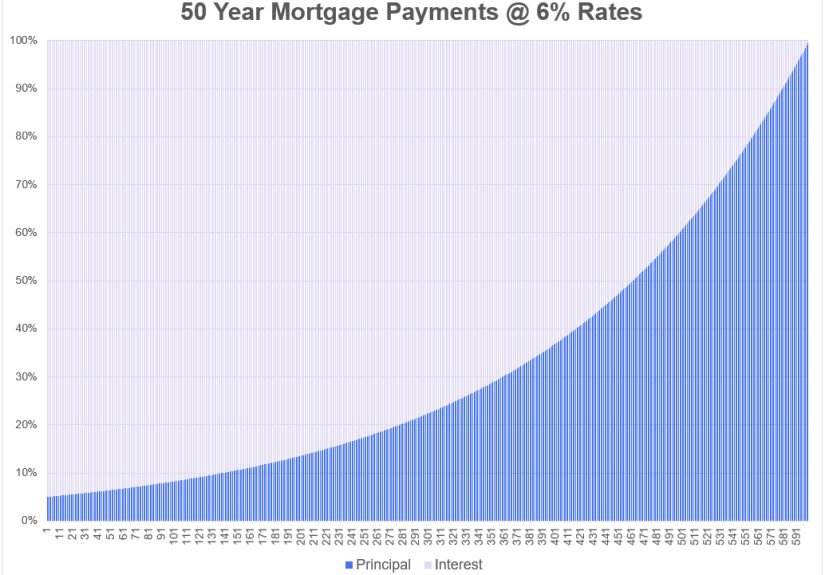

The economics of a 50-year mortgage start with amortization. A mortgage payment is not random. It is built from a formula that spreads principal and interest across a set number of months. When you increase the term from 30 years to 50 years, you move from 360 payments to 600 payments. That instantly lowers the required monthly payment because the debt is being stretched over a much longer period.

Here is the catch: early mortgage payments are heavily weighted toward interest. So when you add 20 more years, you are not merely giving yourself extra time. You are buying a much longer period of interest-heavy repayment.

A clean example

Using a loan amount of $400,000 and a rate of 6.22%, which is close to the average 30-year fixed mortgage rate reported by Freddie Mac on March 19, 2026, the difference is striking:

- 30-year mortgage at 6.22%: about $2,455 per month in principal and interest

- 50-year mortgage at 6.22%: about $2,171 per month in principal and interest

That means the 50-year loan saves roughly $284 per month. At first glance, that sounds meaningful. And for a household on the edge of qualifying, it could feel huge.

Now here comes the anvil:

- 30-year total interest: about $483,825

- 50-year total interest: about $902,564

Yes, you read that correctly. In this example, the longer mortgage adds roughly $418,739 in lifetime interest to save about $284 a month. That is not a typo. That is the price of dragging your mortgage into what is essentially a second adulthood.

And this example is actually generous to the 50-year mortgage because it assumes the same interest rate as a standard 30-year loan. In real life, a 50-year mortgage in the U.S. would likely carry a higher rate because it would sit outside the standard Qualified Mortgage framework and outside the mainstream secondary market. If that same $400,000 loan were priced at 6.75% instead, the monthly payment would be about $2,331, and total interest would approach $998,302. Suddenly the monthly savings shrink, while the long-term cost balloons even more.

Equity Growth: The Hidden Cost Nobody Brags About

Most mortgage shoppers focus on one number: the monthly payment. That is understandable, but incomplete. The better question is: how quickly do I actually own more of my house?

With the same $400,000 example at 6.22%, the difference in equity build is dramatic:

- After 10 years on a 30-year mortgage: you would have paid down about $63,311 in principal

- After 10 years on a 50-year mortgage: you would have paid down only about $16,188

That is not a small gap. That is the difference between “I am making progress” and “I appear to be renting from my lender with extra paperwork.”

After 20 years, the spread gets even wider:

- 30-year mortgage principal repaid after 20 years: about $181,049

- 50-year mortgage principal repaid after 20 years: about $46,293

Why does this matter? Because home equity is one of the main wealth-building engines for American households. A 50-year mortgage slows that engine to the speed of a sleepy turtle. If home prices rise, you may still build wealth through appreciation, but the debt itself lingers far longer. If prices flatten or fall, the slower principal paydown becomes even more painful.

Why 50-Year Mortgages Are a Bad Fit for the U.S. Mortgage System

The economics of a 50-year mortgage are not just about consumers. They are also about how the U.S. mortgage machine works.

Mainstream American mortgages are designed around a highly liquid secondary market. Lenders originate loans, then often sell them. Fannie Mae and Freddie Mac help create that market by purchasing qualifying mortgages that fit established underwriting standards. Consumer-finance rules also give special treatment to Qualified Mortgages, which generally cannot have loan terms longer than 30 years.

That matters because liquidity lowers costs. Standardization lowers friction. When a product falls outside those channels, lenders usually face more risk, fewer buyers for the loan, and more pricing uncertainty. Guess who tends to pay for that? The borrower.

This is a major reason longer-term mortgages above 30 years remain niche in the U.S. Even 40-year mortgages are generally non-QM products and are often seen more often in loan modifications than in ordinary home purchase financing. A 50-year mortgage would likely be even more specialized, more expensive, and less available.

So while the concept sounds borrower-friendly, the U.S. system gives lenders strong reasons to either avoid the product or charge more for it. That higher rate can erase a surprising amount of the payment benefit that made the loan attractive in the first place.

Would a 50-Year Mortgage Actually Improve Housing Affordability?

This is where the idea starts to wobble. A lower payment can improve payment affordability for an individual buyer. But it does not necessarily improve market affordability.

If more buyers can qualify for the same scarce homes by stretching their loan terms, demand can rise without adding supply. When demand rises faster than supply, sellers tend to respond the way sellers usually do: by asking for more money. In other words, the payment relief may be partly capitalized into higher home prices.

That is why many housing economists point back to supply. If the country is short millions of homes, financing tricks alone cannot solve the problem. They may change who can bid and how much they can bid each month, but they do not create more front doors.

There is also a distribution issue. A 50-year mortgage may help some marginal buyers qualify, but it could do so by encouraging them to accept more debt, slower equity growth, and greater lifetime exposure to interest-rate and income risk. That is not always a path to stable wealth. Sometimes it is just a prettier version of being stretched.

Who Might Actually Benefit?

To be fair, the economics of a 50-year mortgage are not universally terrible in every possible scenario. There are limited situations where a very long term can serve a purpose.

1. Borrowers in distress

In the loan-modification world, stretching a mortgage term can be a practical way to reduce payments and avoid foreclosure. If the choice is between a 40- or 50-year-style workout and losing the home, the math changes. Survival math is not the same as optimization math.

2. Borrowers who intentionally overpay

A borrower could take the required payment of a 50-year mortgage but make extra principal payments as if it were a 30-year loan. That creates flexibility in tough months. The problem is behavioral: most people do not consistently prepay debt for decades just because they theoretically could. Life has a way of spending your good intentions.

3. Households with unusual income patterns

A family expecting higher future income might accept a longer term now to reduce pressure in the early years. But this is risky if the income growth does not arrive on schedule. Hope is not an underwriting model.

For most ordinary buyers, though, the 50-year mortgage is less an elegant solution than an expensive workaround.

Smarter Alternatives to a 50-Year Mortgage

When buyers want lower monthly costs, there are usually better options than turning a home loan into a multigenerational commitment.

- Buy a cheaper home: Not glamorous, but highly effective.

- Increase the down payment: Borrow less, pay less, panic less.

- Use a 30-year mortgage and prepay when possible: This keeps flexibility without locking in 50 years of debt.

- Consider an ARM if you truly expect a shorter holding period: Not for everyone, but sometimes more efficient than a very long fixed term.

- Look for down payment assistance or local first-time buyer programs: Lowering upfront barriers can be more sustainable than extending debt forever.

- Refinance later if rates improve: This is not guaranteed, but it is often a more sensible bet than committing to five decades at a high-cost structure.

The best mortgage is not the one with the smallest required payment. It is the one that balances affordability, risk, flexibility, and long-term wealth-building. Those are not always the same thing.

The Bottom Line

The economics of a 50-year mortgage are easy to summarize and hard to love. Yes, the payment can be lower. But that lower payment often comes at the cost of far more interest, painfully slow equity growth, and a product structure that does not fit neatly inside the standard U.S. mortgage market.

In a country dealing with high home prices, elevated rates, and a housing shortage, a 50-year mortgage can look like relief. In reality, it is often a financing bandage placed over a supply problem. It may help a few borrowers in special situations, especially as a hardship tool, but it is a weak candidate for a mainstream affordability solution.

So if someone tells you a 50-year mortgage is the key to affordable homeownership, the correct response is probably not applause. It is a calculator.

Real-World Experiences With the Economics of a 50 Year Mortgage

In practice, the conversation around a 50-year mortgage usually starts with relief and ends with raised eyebrows. Buyers see the lower monthly payment first because that is the most visible number. It feels concrete. It feels livable. A household that cannot comfortably handle a $2,455 principal-and-interest payment may look at something closer to $2,171 and think, “Finally, a version of this that fits real life.” That emotional reaction is completely understandable. The mortgage is no longer just a theory; it suddenly feels possible.

Then the second wave hits. Buyers begin to realize that the required mortgage payment is only one part of the housing bill. Property taxes still exist. Homeowners insurance still exists. Maintenance definitely still exists, and unlike your lender, your roof does not care about your amortization schedule. Many households discover that the monthly savings from a longer term look much smaller once the full cost of ownership is on the table. The loan helps, but it does not magically turn an expensive home into a cheap one.

Another common experience is the shock of seeing how little principal gets repaid in the early years. People often assume that making payments for a decade must mean they own a lot more of the home. On a very long mortgage, that assumption can be badly wrong. Borrowers who compare amortization tables often describe the experience as sobering. Ten years feels like a long time in life, but in a 50-year loan, it can barely move the needle. That can be frustrating for owners who plan to sell, move up, or tap equity later.

Loan officers and financial planners also tend to notice a behavior gap. Some borrowers say they will take the 50-year mortgage for flexibility and then voluntarily pay extra principal whenever possible. That plan sounds smart. Sometimes it even works for a while. But the real-world pattern is messier. Cars break down. Child care costs rise. Income changes. Medical bills appear out of nowhere like unwanted sequels. The extra-payment strategy is easy to promise and harder to maintain. Over time, many households drift back to the minimum payment, which means the expensive long-term math wins.

There is also the psychological experience of carrying a mortgage that stretches far beyond traditional expectations. A 30-year loan is already long enough to make people joke that they will be paying it off on Mars. A 50-year term changes the time horizon in a way that can feel strange. Buyers start doing the mental math: “How old will I be when this ends?” For some, that realization creates stress rather than comfort. The lower payment solves today’s problem but introduces a new kind of financial fatigue.

Perhaps the biggest practical lesson is this: borrowers do not live in spreadsheets. They live in uncertain careers, changing family sizes, and housing markets that move when they least expect it. The economics of a 50-year mortgage may work in a narrow technical sense, but the lived experience often reveals how fragile the strategy can be. It is not always a disaster. For some households, especially in hardship situations, it can genuinely provide breathing room. But for many would-be buyers, the experience is less “This made homeownership affordable” and more “This made an unaffordable house look temporarily manageable.” That is a very different outcome.

Note: Payment examples above are illustrative principal-and-interest estimates only and do not include property taxes, homeowners insurance, mortgage insurance, HOA dues, maintenance, or closing costs.